Key takeaways

- Indemnity insurance covers a defined legal risk; it does not fix the underlying defect.

- Common policies relate to missing planning consent, building regulation certificates, restrictive covenants, rights of way and absent landlords.

- Contacting the relevant authority before legal advice can sometimes invalidate or prevent cover.

- Landlords should check whether the issue affects letting, licensing, insurance, mortgage terms or future saleability.

- The solicitor, lender and insurer should all be clear on the exact risk before exchange.

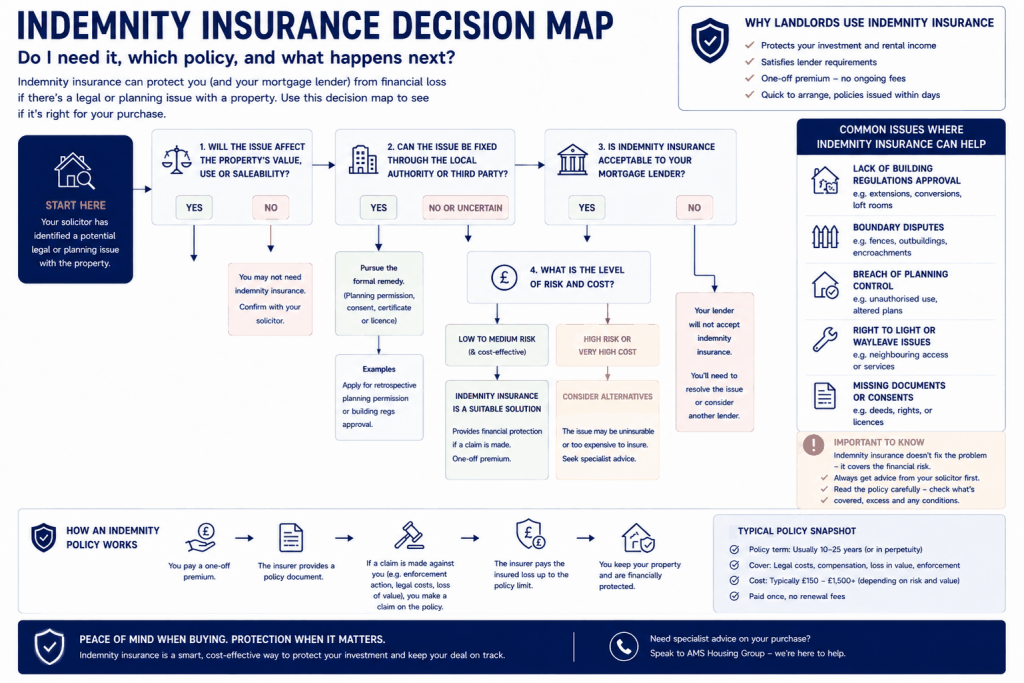

Indemnity insurance is a one-off policy used during conveyancing to cover a specific legal defect or missing document. It can help a purchase proceed when a problem cannot be corrected quickly, but it does not repair the defect itself.

That distinction matters for landlords. A policy for missing building regulation approval may help with a legal enforcement risk, but it does not prove that the works are safe, insurable or suitable for letting. A buyer planning to rent the property still needs to check condition, safety certificates, licensing and lender consent.

This guide explains what indemnity insurance can and cannot do when buying a house, with extra focus on London landlords and buy-to-let buyers.

What indemnity insurance actually covers

The policy is usually designed to protect against financial loss if a third party takes enforcement action or asserts a right connected to the defect. It is not a guarantee that the property is sound. It is not a building survey. It is not confirmation that works comply with current standards.

A policy might be used where building regulation completion paperwork is missing, a restrictive covenant may have been breached, a planning document cannot be located, an easement is unclear or a freeholder is absent. The cover depends on the wording, not on the broad policy name.

For a buyer, the key question is whether the legal defect is acceptable. For a landlord, there is a second question: can the property still be lawfully and safely let after completion?

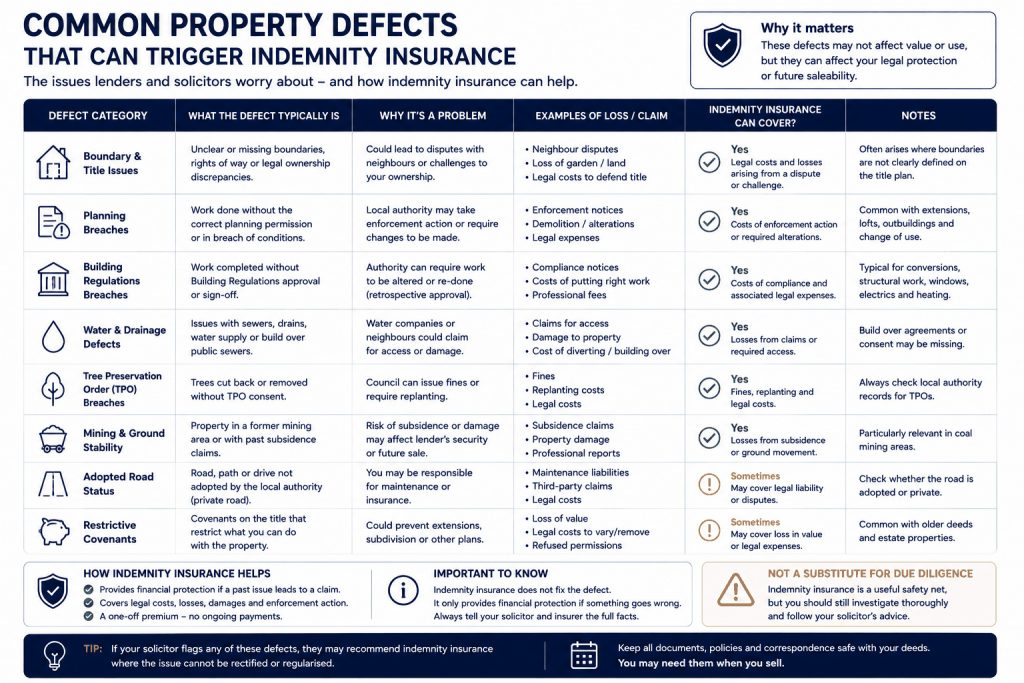

The common defects that trigger it

The most common triggers are missing building regulation approval, missing planning consent, lack of listed building documentation, chancel repair liability, restrictive covenant risk, lack of right of way evidence, absence of a landlord in a leasehold title and missing FENSA or boiler paperwork.

Some of these are administrative. Others can change the risk of owning, selling or letting the property. A missing FENSA certificate is not the same as a loft conversion with no evidence of structural approval. A narrow title defect is not the same as a covenant preventing subletting.

Buyers should not let the word insurance soften the investigation. Ask why the policy is being proposed, what risk it excludes and whether the lender is satisfied.

Why landlords should be more careful than owner-occupiers

An owner-occupier may decide that a small legal defect is acceptable because they plan to live in the property and do not need a licence or tenant occupation route. A landlord has more moving parts: mortgage consent, landlord insurance, Right to Rent processes, deposit rules, safety certificates, local licensing and future saleability.

A policy for missing building regulations may protect against enforcement but still leave a landlord with an unsafe staircase, poor fire separation or an extension that makes the property unsuitable for HMO use. Insurers, councils and future buyers may all ask different questions.

Before exchange, buy-to-let buyers should speak to their solicitor and, where the issue affects letting risk, consider legal and financial property advice (/legal-financial-property-advice/) or a rental property compliance inspection (/compliance-inspection/).

When insurance is not enough

Insurance is usually not enough where the issue is a present safety problem, an active enforcement dispute, a clear lease breach, a lender refusal, a known neighbour objection, a defective conversion or a condition that prevents lawful occupation. In those cases, a policy may not respond, or it may be irrelevant to the real problem.

Be careful with authority contact. Some indemnity policies rely on the risk not having been put in front of the council, freeholder, church body or other third party. Contacting them before solicitor advice can make cover unavailable or invalid. That does not mean silence is always right; it means the solicitor should guide the route.

If the property is in London, also check borough licensing before completion. A property that is mortgageable may still need costly works before it can be legally let.

Questions for your solicitor

Ask what exactly is being insured, who is protected, how long the policy lasts, whether successors in title are covered, whether the lender accepts the policy, and what actions could invalidate the cover. Ask whether the policy covers only enforcement cost or also loss in property value.

For a rental purchase, add landlord questions: does the defect affect subletting, HMO licensing, fire safety, future rentability, insurance or a later resale? Should the price be renegotiated? Is a retention or remedial work better than a policy?

The best answer is sometimes to proceed with a policy. Sometimes it is to renegotiate. Sometimes it is to walk away. The policy should support the property decision, not replace it.

How it affects future sale or letting

A policy that satisfies today’s lender may not remove tomorrow’s buyer concern. Future buyers, surveyors or lenders may ask why the policy was needed and whether the underlying issue has worsened. If the defect affects layout, fire safety or access, it can come back during a sale or remortgage.

Landlords buying with a letting plan should compare the purchase risk with the intended income route. AMS can help through property sales support (/property-sales/), portfolio review for landlords (/portfolio-review/) and property management support if the property will be retained.

A London landlord purchase example

Imagine buying a leasehold flat in Waltham Forest with a small rear alteration and missing completion paperwork. The seller offers an indemnity policy and the lender accepts it. That may be enough to complete the purchase, but it does not answer whether the alteration affects ventilation, escape route, damp risk or future letting suitability.

If the flat will be let, the buyer should ask whether the policy protects only against enforcement or whether a tenant, council officer, insurer or future buyer could still raise the condition of the works. A missing certificate can be a paperwork issue. It can also be a warning that nobody checked the work properly.

This is why landlord buyers should connect conveyancing with management reality. The cheapest way to finish a purchase can become expensive if the property then needs remedial works before it can be let.

How lenders and future buyers may view it

A lender may accept an indemnity policy for a specific defect today, but that does not mean a future buyer or future lender will view the same issue the same way. Lending policies change, property condition changes and the defect may become more obvious after inspection.

If the defect affects a leasehold consent, loft conversion, access, drainage or building regulations, future saleability should be part of the negotiation. A policy is useful only if it protects the risk that actually matters.

Ask the solicitor to explain the practical resale position in writing. If the property is likely to be sold as an investment later, make sure the issue will not narrow the buyer pool.

How AMS would test the policy against letting plans

For a landlord buyer, AMS would not start with the policy price. The first question is what the buyer wants to do with the property. A defect that is acceptable for owner occupation may be more serious if the plan is to let to a family, create a company let, use the property as an HMO or sell to another investor later.

The next question is whether the defect affects compliance. If it touches fire safety, damp, access, planning, lease consent or a structural alteration, the policy should be considered alongside survey advice and a letting-readiness inspection. Insurance may cover enforcement loss but not repair cost or lost rent during remediation.

The safest position is a written note from the solicitor explaining the defect, the policy, the restrictions and the likely impact on mortgage, letting and resale. Without that, the buyer is relying on a product they may not fully understand.

Indemnity policy risk check

| Issue | Landlord question |

| Missing building regulations | Is the work physically safe and suitable for letting, not just insurable? |

| Restrictive covenant | Could it restrict subletting, HMO use, alterations or parking? |

| Absent freeholder | Will this slow lease extension, consent, repairs or resale? |

| Planning issue | Is the enforcement risk timed out, ongoing or still active? |

| Unknown right of way | Could access, bins, parking or tenants be affected? |

FAQs

Who usually pays for indemnity insurance?

It is negotiable. In many transactions the seller pays because the defect relates to the property being sold, but the buyer may agree to pay to keep the transaction moving.

Does indemnity insurance make a property safe?

No. It covers a defined financial/legal risk. It does not confirm that building work is safe or compliant.

Can I contact the council before taking a policy?

Do not contact the authority before speaking to your solicitor. Contact can sometimes invalidate or prevent cover.

Does the policy last forever?

Many conveyancing indemnity policies are one-off and last indefinitely, but the exact duration and who is covered depends on the wording.