Key takeaways

- Right to Buy is still available in England, but the November 2024 discount caps make the calculation much tighter than older articles suggest.

- For London buyers, the hidden risk is often leasehold cost: service charges, section 20 major works, repairs and resale restrictions can outweigh the headline discount.

- Selling within five years normally means repaying some or all of the discount, and selling within ten years can trigger the council or former landlord right of first refusal.

- Letting the home after purchase is not automatic. The buyer must check the lease, mortgage conditions, insurance and local landlord licensing before treating it as a rental asset.

- AMS should position this page as a practical Right to Buy ownership-risk guide, with internal links to property sales, landlord licensing and valuation support rather than competing with service pages.

Buying a council house with new rules is not just a question about eligibility. In 2026, the bigger question is whether the home still makes sense once you add the reduced Right to Buy discount, mortgage affordability, leasehold charges, future resale limits and any plan to let the property later.

For a secure council tenant who wants to live in the home long term, the answer may be positive. For a buyer thinking, “I will buy now and rent it out later”, the answer needs much more care. A discounted purchase can become expensive if the lease restricts subletting, the lender will not consent to letting, or the service charge rises after major works.

AMS Housing Group is based in Barking and works across all 33 London boroughs and Essex. Where a Right to Buy purchase is part of a wider property plan, our property sales support and landlord advice can help compare the open-market sale, future letting and long-term ownership routes before the buyer commits.

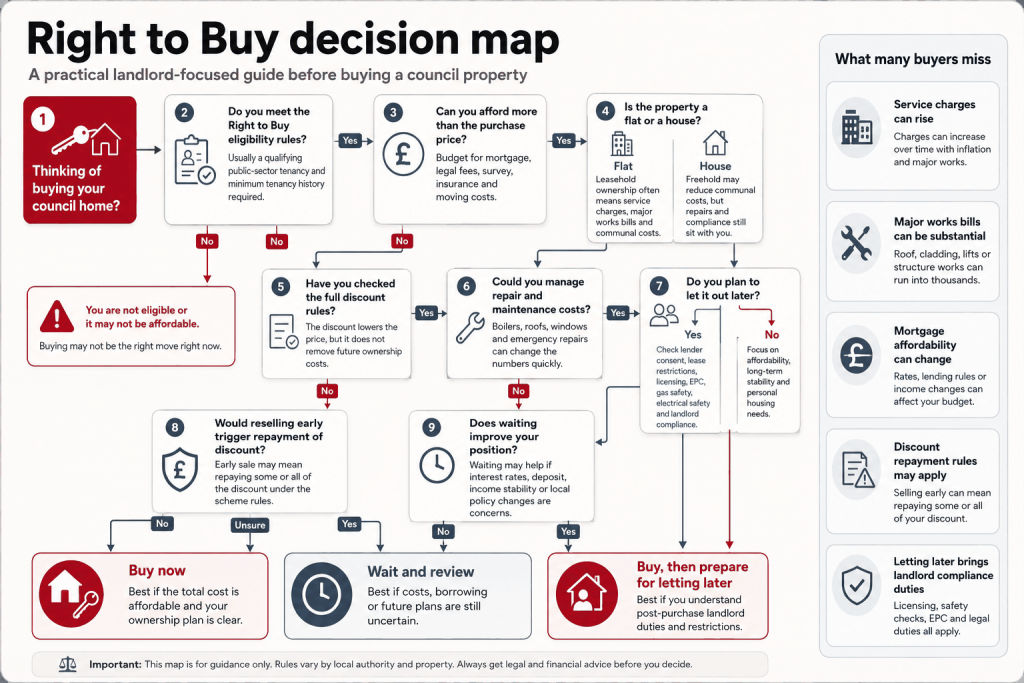

How Right to Buy works in England in 2026

Right to Buy allows most eligible council tenants in England to buy their council home at a discount. The core eligibility test is still property-specific. GOV.UK says the home must normally be the tenant’s only or main home, self-contained, held by a secure tenant, and the tenant must have had a public sector landlord for at least three years. Those three years do not have to be consecutive.

The keyword here is “most”. Housing association tenants may have a Preserved Right to Buy only if the home used to be council-owned and was transferred while they lived there. Some homes and circumstances fall outside the basic route. A buyer should ask the landlord for the formal position rather than relying on what a neighbour was told.

This is the right place for a decision-map visual. Readers need to see that Right to Buy is not a single yes-or-no question: eligibility, discount cap, mortgage terms, leasehold exposure and future letting plans all sit in the same decision chain.

| Right to Buy check | Why it matters before applying |

| Secure tenancy and main home | A buyer usually needs to occupy the property as their only or main home. A plan to buy purely for investment can conflict with lender, lease and scheme expectations. |

| Public sector tenancy history | Eligibility depends on qualifying public sector tenancy time. Joint applications use the longest qualifying tenant history. |

| Flat or house | Flats and houses have different discount formulas and very different future cost profiles. |

| Preserved Right to Buy | Some ex-council housing association homes qualify, but the landlord must confirm the position. |

| Leasehold restrictions | Many council flats are leasehold and can carry service charge, major works and subletting restrictions. |

Right to Buy discounts after the November 2024 reduction

The major update many older articles miss is the reduced regional discount cap for applications made from 21 November 2024. GOV.UK now sets regional maximum discounts, with London generally capped at £16,000, except Barking and Dagenham and Havering where the cap is £38,000. That is a very different calculation from the previous London cap of £136,400 for applications made before 21 November 2024.

The percentage formula still matters, but it is capped. For houses, the discount starts at 35% after three to five years as a public sector tenant, then rises by 1% for each extra year after five years. For flats, it starts at 50%, then rises by 2% for each extra year after five years. In both cases, the discount cannot exceed 70% of the property value or the regional cash cap, whichever is lower.

| Property and timing | Current practical impact |

| London application after 21 November 2024 | Maximum discount usually £16,000, except Barking and Dagenham and Havering at £38,000. |

| Application before 21 November 2024 | Old caps may apply: £136,400 in London or £102,400 outside London, subject to the rules. |

| House discount formula | 35% after three to five years, then 1% extra per year after five years, capped. |

| Flat discount formula | 50% after three to five years, then 2% extra per year after five years, capped. |

| Landlord spending on the home | A smaller or no discount may apply if the landlord has spent heavily on the property. |

This changes the tone of the decision. A £16,000 discount on a London flat is still useful, but it will not rescue a weak affordability position. Buyers should run the mortgage on the full cost of ownership, not on the emotional pull of a discount.

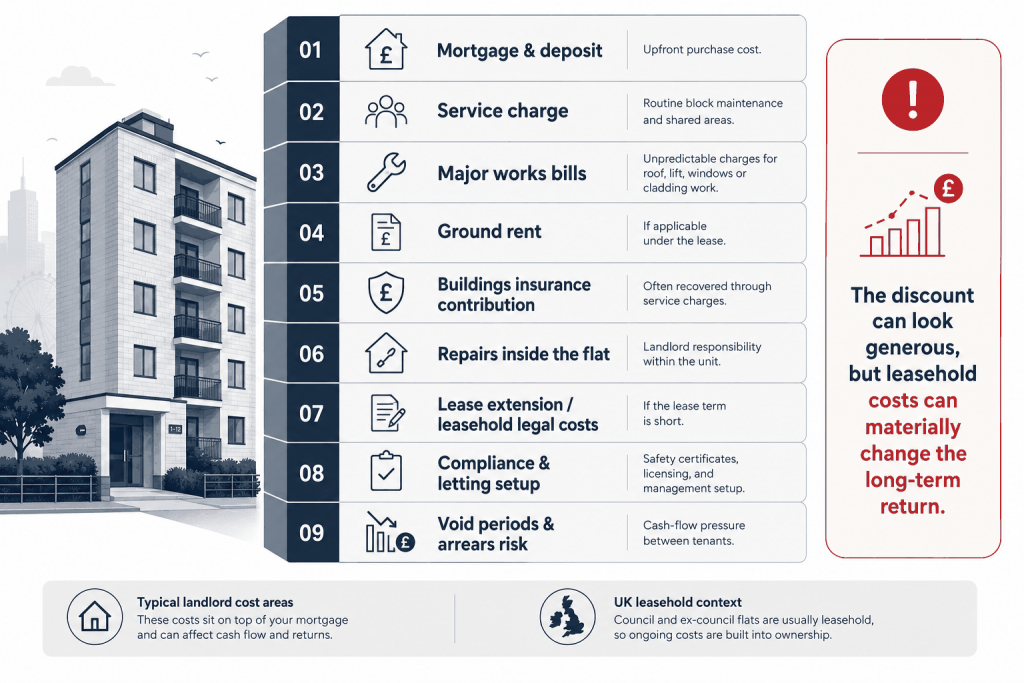

The council flat cost most buyers underestimate: major works

Council flats can be attractive because the purchase price is often below nearby open-market homes, even after reduced discounts. The problem is that leasehold ownership moves repair liability into a different shape. A leaseholder pays service charges and may receive major works bills for roof repairs, lifts, windows, fire safety work, estate improvements or external decorations.

In London, older blocks can produce large one-off bills. A Right to Buy purchaser who focuses only on the mortgage may be shocked when the first section 20 consultation lands. This is especially important in boroughs with post-war estates and older council stock, including Barking and Dagenham, Newham, Waltham Forest, Tower Hamlets and Southwark.

- Ask for service charge accounts for the last three years, not just the current estimate.

- Ask whether any section 20 major works consultation has started or is planned.

- Check whether the building has lift, roof, cladding, fire safety or estate works in the pipeline.

- Ask the solicitor to explain subletting, alteration and sale restrictions in plain English.

- Build a cash reserve before completion. A discounted price does not remove the need for repairs.

Use the image here to make the leasehold cost stack visible. The section explains the problem in words; the image should show how a low purchase price can sit above recurring and one-off costs that affect the real five-year position.

Selling a Right to Buy home within five or ten years

A Right to Buy purchase is not always clean to exit. GOV.UK says a buyer who sells within five years of buying must repay some or all of the discount. The repayment is all of the discount in year one, then 80% in year two, 60% in year three, 40% in year four and 20% in year five. The repayment is linked to the value at resale, not simply the original discount amount.

There is also a first-refusal rule. If the owner sells within ten years of buying through Right to Buy, they must first offer the home back to their old landlord or another social landlord in the area. If that landlord does not agree to buy within eight weeks, the owner can sell on the open market.

This matters for anyone buying with a plan that might change. A job move, family change, mortgage stress or repair bill can force a sale earlier than expected. A five-year discount clawback and ten-year offer-back period should therefore be treated as part of the cost of buying.

Can you rent out a council house after buying it?

There is no simple national answer that every buyer can rely on. After completion, the home is privately owned, but the practical ability to let it depends on the mortgage, lease, insurance, local licensing and any restriction in the purchase paperwork. A buyer who says “I will rent it out later” should check that plan before applying, not after completion.

The mortgage is often the first barrier. A residential mortgage usually assumes the owner will live in the property. Letting the home later may require consent to let or a remortgage onto a buy-to-let product. A lender can refuse, charge a higher rate or set conditions. If the property is a leasehold flat, the lease may also require consent to sublet.

If the plan is to become a landlord later, compare the property with AMS lettings support for landlords before assuming the home will work as a straightforward rental.

Place a rental-readiness checklist image after this section. It should support the point that a former council home only becomes a safe rental asset after lease, lender, insurance and local licensing checks line up.

When buying makes sense – and when waiting is safer

Buying can make sense where the buyer intends to live in the home long term, can afford the mortgage after stress testing, understands the lease and has a reserve for repairs. It is weaker where the buyer is relying on short-term resale, has no repair reserve, or is stretching affordability simply because a discount is available.

A useful test is to run three versions of the numbers. First, the happy path: mortgage affordable, service charges stable, no major works. Second, the pressure path: mortgage rate increases at renewal, service charge rises, boiler or roof work is needed. Third, the exit path: the owner needs to sell within five years and repays part of the discount.

If all three versions still work, the purchase may be sensible. If the plan only works in the happy path, the buyer should slow down.

Borough examples: Barking flat, Waltham Forest maisonette and Havering house

A Barking and Dagenham flat may benefit from the higher current discount cap compared with most London boroughs, but the block condition and future service charges may carry more weight than the discount. If the estate has planned roof, lift or fire-safety works, the buyer needs those numbers before completion.

A Waltham Forest maisonette can look more flexible, but lease terms and selective licensing need checking if the owner later wants to let. The Elizabeth line, Overground or tube access nearby can support demand, but it does not remove the legal steps.

A Havering house can be cleaner from a leasehold perspective if it is freehold, but the rental plan still depends on mortgage consent, licensing status and achievable rent. The property may be easier to manage as a family let than as a multi-let, depending on layout and local demand.

Documents to gather before applying for Right to Buy

- Your tenancy agreement and any letters confirming secure tenancy status.

- The Right to Buy application paperwork and landlord offer notice once issued.

- Service charge accounts, planned works notices and any section 20 consultation documents for flats.

- Mortgage agreement in principle, including any conditions about future letting.

- Lease summary from a solicitor explaining subletting, alterations, repairs and resale rules.

- Insurance quotes for owner occupation and, if relevant, future landlord cover.

- A simple five-year budget showing mortgage, service charge, repairs, resale restrictions and emergency reserve.

How AMS would review the decision

When AMS reviews a property decision, we do not start with the biggest headline number. We start with what the owner wants the property to do. A home bought to live in is judged differently from a home that may later be rented, sold, inherited or remortgaged.

For a landlord-minded buyer, the question is not “Can I buy it?” The question is “Will the property still work after the purchase rules, lender conditions, repair liabilities and rental regulations are included?” That is where many Right to Buy decisions become clearer.

For a property-specific view, request a free property valuation from AMS or speak to our team on 020 3793 2247 before building a landlord plan around a discounted purchase.

AMS checks for Right to Buy buyers planning to let later

If the purchase may later become a rental or sale asset, the safest route is to test the lease, mortgage and licensing position before completion.

For legal structure, lease and mortgage questions, use AMS legal and financial property advice alongside a qualified solicitor.

For owners with more than one property or a future buy-to-let plan, an AMS portfolio review for landlords can show whether the numbers work across the whole portfolio.

If you need a human conversation before applying, contact AMS Housing Group and ask for the property sales or landlord advice team.

Frequently asked questions about buying a council house new rules

What are the new Right to Buy discount rules in 2026?

For applications made from 21 November 2024, Right to Buy maximum discount caps are much lower than before. London is generally capped at £16,000, except Barking and Dagenham and Havering where the cap is £38,000. The percentage formula still applies, but the lower cash cap often decides the final discount.

Can I sell a Right to Buy home straight away?

You can sell, but selling quickly can trigger restrictions. If you sell within five years, you usually repay some or all of the discount. If you sell within ten years, you must first offer the property to your old landlord or another social landlord in the area.

Can I rent out a council house after buying it?

Possibly, but only after checking the mortgage, lease, insurance and local licensing rules. A residential lender may require consent to let. A lease may restrict subletting. A London borough may require selective licensing or HMO licensing depending on how the property is let.

Is Right to Buy still worth it after the discount reduction?

It can be, but the decision is now more dependent on the property’s long-term costs. The lower discount means mortgage affordability, service charges, major works and future plans matter more than they did when higher discount caps applied.

Before you apply, test the full ownership plan

A Right to Buy discount is useful only if the whole ownership plan works. Do not rely on the discount alone. Check the lease, lender, service charges, resale rules and any future letting plan before committing.

This article provides general information only and is not legal, mortgage or tax advice. For a property-specific decision, speak to a qualified solicitor, mortgage adviser or accountant, and use AMS where the question depends on rent, management, compliance or sale strategy.