Key takeaways

- Buying with no deposit is possible only in limited cases. The risk normally moves to a stricter lender assessment, a guarantor, family savings or higher monthly costs.

- A 100% mortgage can reduce the deposit barrier, but it does not remove legal fees, surveys, moving costs, insurance, repairs or the risk of negative equity.

- Rent-history products can help some long-term renters, but they still rely on affordability, credit profile, property type and lender criteria.

- Shared ownership, gifted deposits and guarantor structures can lower the first cash step, but each has restrictions that need proper mortgage and legal advice.

- For AMS, this article should lead readers towards a property-specific affordability and valuation conversation, not promise that no-deposit buying is easy.

Buying a house with no deposit is possible in the UK in 2026, but only for a narrow group of buyers and usually with stricter checks than a standard mortgage. The missing deposit does not remove risk. It moves risk into the mortgage rate, the lender’s criteria, a family member’s finances, or the buyer’s exposure to negative equity.

For London buyers, the question is sharper because prices are higher and flats are common. Some high loan-to-value products exclude flats, new-build homes, self-employed applicants or certain property types. That means a product that looks useful nationally can be hard to use on a typical London flat.

AMS is not a mortgage broker. Our role is property-side advice: rental valuation, sale strategy and whether a property works as a long-term asset. If you are comparing buying against staying in rented accommodation or later becoming a landlord, start with a free AMS property valuation and take mortgage advice from a regulated broker.

What buying with no deposit really means

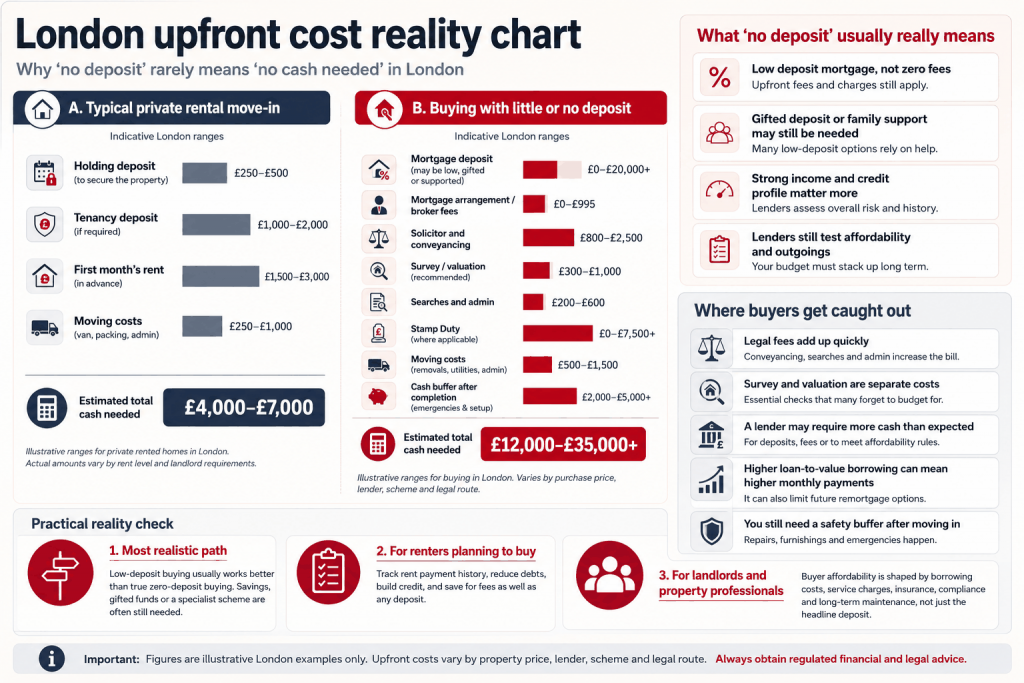

No-deposit buying usually means a 100% loan-to-value mortgage, a family-backed mortgage, a concessionary purchase, shared ownership with a very small cash deposit, or a lender product that uses rent history as evidence of payment discipline. It does not mean buying without costs.

The buyer still needs money for legal fees, survey, mortgage valuation, moving costs, buildings insurance from exchange, initial repairs, furniture and a safety buffer. A buyer who has no deposit and no emergency reserve is usually more exposed than a buyer with a smaller mortgage and cash left after completion.

| Route | How it can reduce upfront deposit | Risk to check first |

| 100% mortgage | Buyer borrows the full property price if they meet strict criteria. | Higher interest rate, negative equity risk and limited lender choice. |

| Family deposit or guarantor product | Family savings or property equity support the loan. | Family member may lose access to savings or carry liability if payments fail. |

| Rent-history mortgage | Payment record helps prove affordability. | Rent history does not replace stress testing or repair reserves. |

| Shared ownership | Deposit is based on the share bought, not the full property value. | Rent on remaining share, service charge and staircasing rules. |

| Lifetime ISA saving route | Government bonus helps build a deposit faster. | Property price cap and withdrawal rules apply. |

Why 100% mortgages are back but still limited

After years of tighter lending, the UK market has seen more low-deposit and no-deposit options return. The important point is that lenders have not returned to the loose pre-2008 model. Modern no-deposit products usually use strict criteria, affordability checks and property restrictions.

Recent high loan-to-value news illustrates the pattern. Some products require a minimum deposit rather than no deposit. Some exclude flats or new-builds. Others are aimed only at first-time buyers with strong incomes and clean credit. That can exclude many London buyers because flats make up a large share of the realistic first-purchase market.

The higher the loan-to-value, the smaller the buyer’s protection if prices fall. If a buyer purchases at £350,000 with no deposit and the property value falls by 5%, the home may be worth £332,500 while the mortgage balance is still close to the original loan. That is negative equity. It can make remortgaging, selling or moving harder.

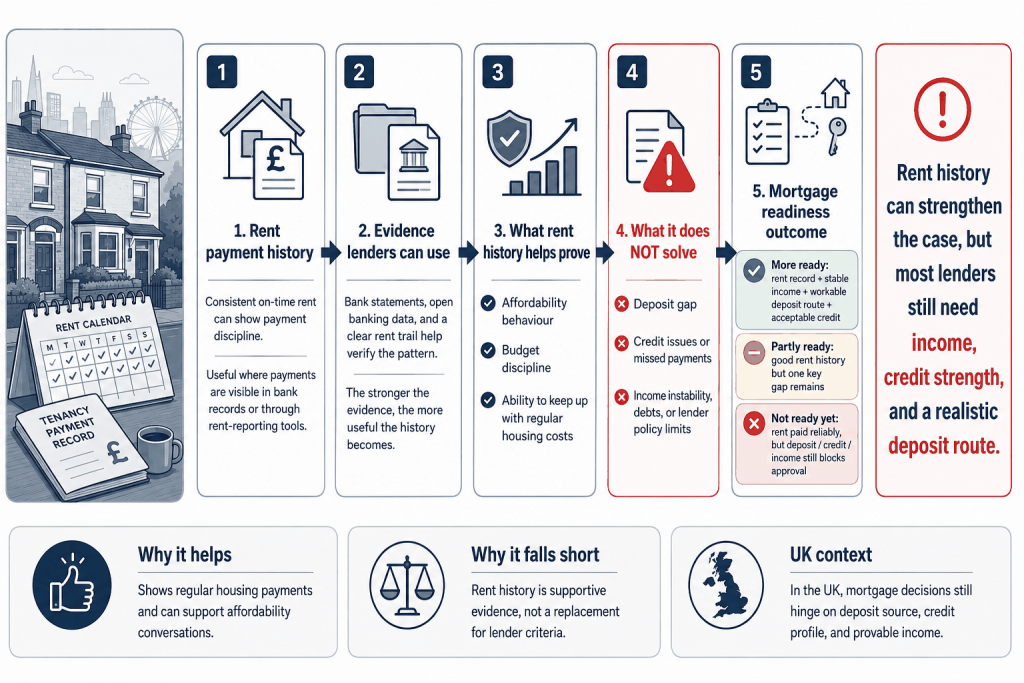

London affordability: rent history is not enough on its own

Rent history can help prove that a buyer has managed monthly payments. It does not prove that the buyer can handle ownership costs. Rent does not usually include building insurance, leasehold service charges, mortgage rate changes, emergency repairs or solicitor costs.

A renter paying £1,600 pcm in Barking may feel ready for a similar mortgage payment. The ownership calculation still needs to include service charge if it is a flat, council tax, insurance, boiler or appliance costs, mortgage renewal risk and a buffer for voids if the property might later be let.

| Ownership cost | Why it matters for a no-deposit buyer |

| Mortgage payment | Higher loan-to-value usually means higher monthly cost than a lower-risk mortgage. |

| Service charge | Leasehold flats can carry ongoing charges and major works bills. |

| Survey and legal fees | These must usually be paid upfront and cannot be ignored because there is no deposit. |

| Repairs reserve | A first boiler, roof or electrical issue can destabilise a buyer with no savings left. |

| Remortgage risk | If values fall or rates rise, switching lender can be harder. |

Family-backed mortgages: the hidden risk for parents and relatives

Family support can be useful, but the risk must be named clearly. A parent may be asked to place savings in a linked account, charge their own home, or act as guarantor. The buyer sees the benefit. The family member carries part of the downside.

Before anyone signs, the family should ask how long the money is locked away, whether interest is paid, what happens if the buyer misses payments, whether the parent’s own remortgage plans are affected and what independent legal advice is required.

- Do not let family support proceed without independent advice for the family member providing security.

- Ask whether the arrangement affects the relative’s own borrowing or retirement plans.

- Check what happens if the buyer wants to sell early, split up with a co-owner or move for work.

- Keep written records. Family agreements become much harder when they rely on memory.

Shared ownership is low deposit, not always low cost

Shared ownership can reduce the deposit because the buyer purchases a share of the property rather than the whole property. A 5% deposit on a 25% share of a £400,000 home is much smaller than a 5% deposit on the full £400,000. That is why it can help buyers who are blocked by deposit size.

The trade-off is that the buyer pays rent on the share they do not own, plus service charge where applicable. Staircasing, resale rules, lease terms and repair responsibility need checking. In London blocks, service charge can be the number that changes the decision.

If you are comparing shared ownership against buying an open-market property that may later be rented or sold, AMS property sales support can help with the property-side numbers, but mortgage and scheme advice should come from regulated specialists.

Lifetime ISA and deposit saving: slower but safer for many buyers

A Lifetime ISA can help first-time buyers build a deposit. GOV.UK says eligible savers can put in up to £4,000 each year and receive a 25% government bonus, up to £1,000 a year. The account is for first-home purchase or later life, and withdrawals outside the rules can create a charge.

For many buyers, a 12-24 month saving plan is less exciting than a no-deposit headline, but it can produce a better mortgage choice, lower interest cost and less negative-equity risk. A buyer who saves a 5% or 10% deposit often has more lender options than someone relying on a narrow 100% product.

| Purchase price | 5% deposit | 10% deposit | Why the deposit changes risk |

| £300,000 | £15,000 | £30,000 | Lower loan-to-value can improve lender choice and rate options. |

| £400,000 | £20,000 | £40,000 | A bigger deposit gives more protection if prices dip. |

| £500,000 | £25,000 | £50,000 | London buyers need to check property caps on schemes before planning. |

When buying with no deposit can make sense

It can make sense where the buyer has stable income, clean credit, predictable employment, no expensive short-term commitments, a property that the lender accepts and cash available for the non-deposit costs. It is more likely to work for someone who has paid rent reliably for years but has been blocked by the deposit barrier.

It is weaker where the buyer is already stretched, has no emergency savings, is buying a property with uncertain service charge, or plans to move within a short period. A no-deposit mortgage is not built for speculative property decisions.

When waiting is the more sensible route

Waiting may be safer if it allows the buyer to build a deposit, clear unsecured debt, improve credit score or understand the target area better. This is particularly true in parts of London where prices, service charges and transport-linked premiums make small mistakes expensive.

A six-month delay that produces a cleaner mortgage application, a survey budget and a repair reserve can be better than rushing into a high loan-to-value loan with no room for error.

If the property may later become a rental

Some buyers ask about no-deposit buying because they eventually want to keep the home as an investment. That plan needs lender consent, landlord insurance, licensing checks, gas and electrical safety certificates, deposit protection, Right to Rent checks and ongoing management.

If your future plan includes letting the property, read AMS guidance on full property management in London before assuming the home will be easy to rent out.

A property that works as a home does not always work as a rental. A leasehold flat with high service charge may have weak yield. A house with good family demand may be easier. A possible HMO needs licence, layout and planning checks. The future landlord plan should be tested before purchase, not after the mortgage completes.

Questions to ask before applying for any low-deposit product

- What is the full monthly payment at today’s rate, and what would it be if rates rose by 1% or 2%?

- What property types are excluded: flats, new builds, ex-local authority blocks or high-rise buildings?

- What cash do I need for solicitor, survey, broker, moving and immediate repairs?

- How would I cope if the property value fell and I could not remortgage easily?

- Does the mortgage allow future letting, or would I need consent to let or a new mortgage?

- Is a family member taking risk, and have they had independent advice?

AMS property checks before a no-deposit purchase becomes an investment

A no-deposit mortgage decision is made by the lender, but the property still needs a separate landlord test if it might later be let or sold.

For legal, ownership and tax questions around future use, speak to AMS about legal and financial property advice as part of the wider property plan.

If the home could become a managed rental later, compare the route with AMS lettings support and understand the setup costs before purchase.

If you already own property and are stretching into another purchase, use an AMS portfolio review before taking on more debt.

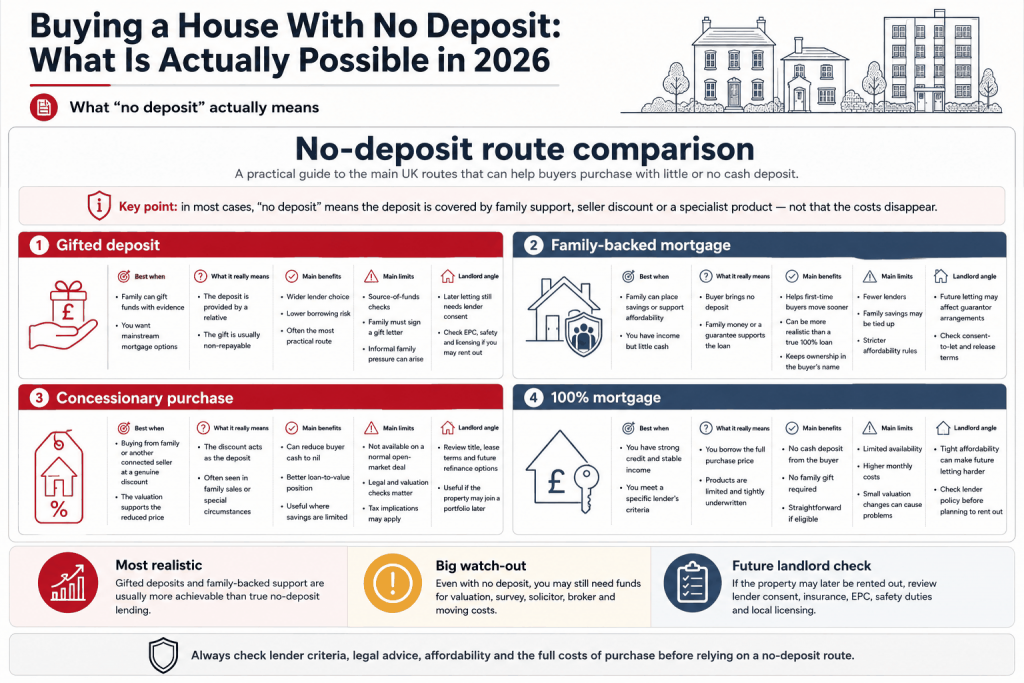

The image should clarify a common misunderstanding: no deposit does not mean no cost. Place a route-comparison visual here so readers can compare the main ways buyers try to reduce the initial cash barrier.

The image should clarify a common misunderstanding: no deposit does not mean no cost. Place a route-comparison visual here so readers can compare the main ways buyers try to reduce the initial cash barrier.

Frequently asked questions

Can you still get a 100% mortgage in the UK?

Yes, some lenders offer or have recently offered 100% or very high loan-to-value mortgages, but availability changes and eligibility is strict. Buyers should use a regulated mortgage adviser and check the product criteria, rate, property restrictions and negative-equity risk.

Is buying with no deposit the same as buying with no upfront costs?

No. A buyer still needs money for legal fees, survey, valuation, moving costs, insurance, furnishings and repairs. Some costs may be rolled into wider planning, but the buyer should not rely on a zero-deposit mortgage if they have no cash buffer at all.

Can rent history help me buy a house?

It can help with some lender products, but rent history is not the whole affordability test. Lenders still look at income, credit commitments, spending, property type and stress-tested repayments.

Is no-deposit buying risky in London?

It can be. London prices, leasehold flats and service charges mean the buyer has less room for error. The risk is not that no-deposit mortgages are automatically bad; it is that the buyer has very little equity if prices fall or costs rise.