Key takeaways

- Estate agent fees are usually the largest visible selling cost and should always be checked with VAT included.

- Conveyancing is usually higher for leasehold and tenanted sales because extra documents and enquiries are needed.

- Sellers need an EPC before marketing unless a valid certificate already exists or an exemption applies.

- Mortgage early repayment charges and possible Capital Gains Tax can change the decision entirely.

- Landlords should compare net sale proceeds with future rental income before assuming sale is the best route.

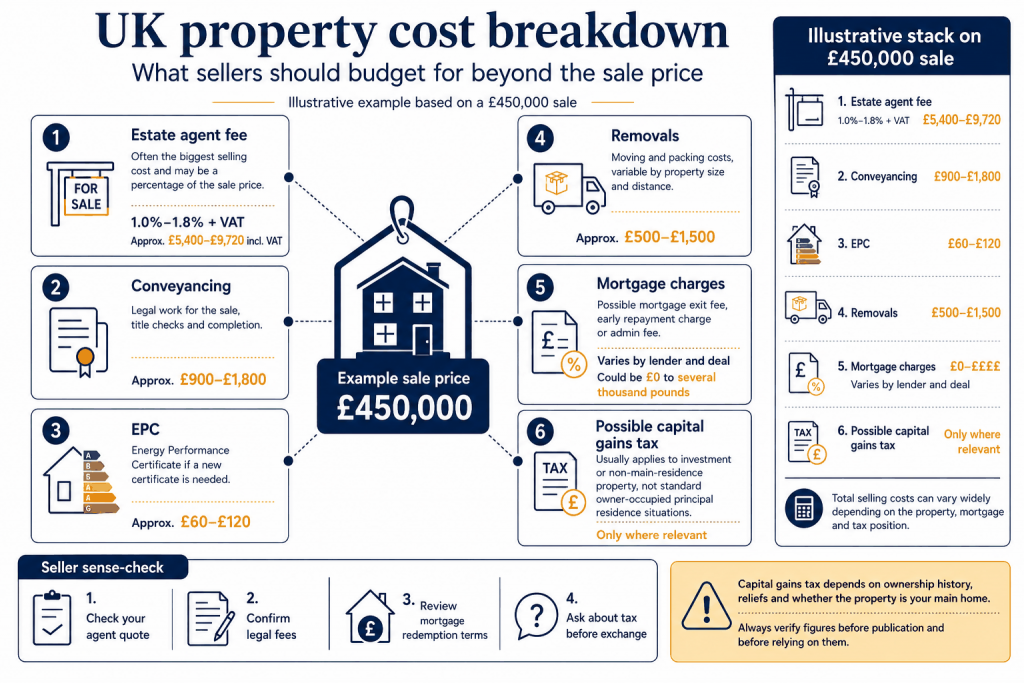

For many UK sellers, the core cost of selling a house sits around £5,000 to £15,000 before early repayment charges, major repairs, removals or tax. On a £450,000 London property, an estate agent fee of 1.2% plus VAT is £6,480 before legal costs or moving costs are added.

The true figure depends on property value, freehold or leasehold status, mortgage terms, presentation costs and whether the property is a main home, second home or buy-to-let. Landlords need one more calculation: the income they give up by selling.

This article gives a full cost picture and helps landlords compare selling with property sales support, portfolio review and guaranteed rent.

House selling fees UK: the costs most sellers should budget for

A realistic selling budget separates mandatory costs, professional fees, optional preparation costs and tax. A mortgage-free homeowner selling a main residence may pay the agent, solicitor, EPC and removals. A landlord selling a leasehold buy-to-let can add leasehold pack fees, redemption charges and possible Capital Gains Tax.

GOV.UK says sellers must order an EPC before marketing. GOV.UK also warns that estate agent contracts are legally binding, so sellers should check fees, VAT, sole agency periods and withdrawal terms before signing.

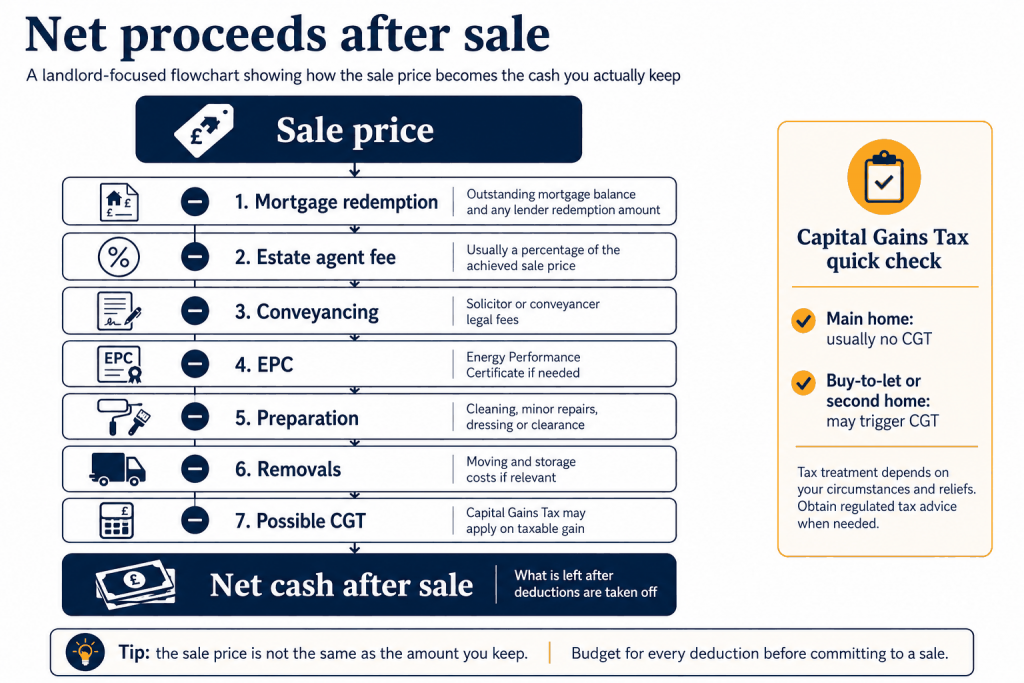

For landlords, the key number is not sale price. It is net proceeds after mortgage, selling costs, tax and lost future income.

Estate agent and conveyancing costs

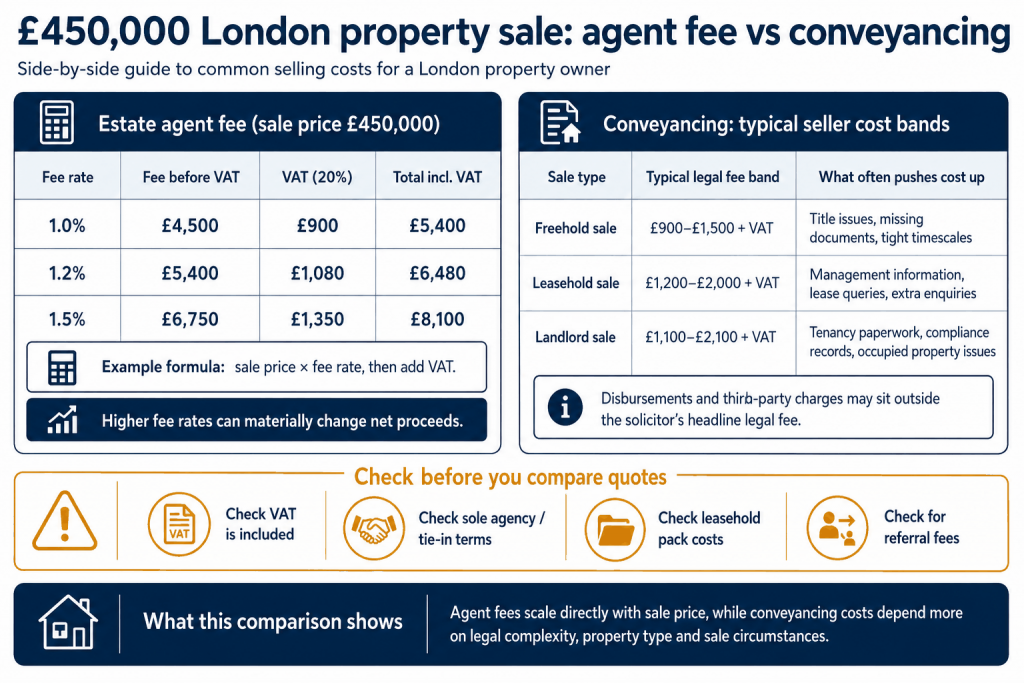

High-street estate agent fees are commonly percentage-based. A small percentage difference can mean thousands of pounds on a London sale. Compare service, local buyer database, sales progression and contract terms, not just the headline percentage.

Conveyancing costs depend on complexity. Leasehold sales, tenanted sales, shared ownership, probate, title defects and missing documents usually need more work. A cheap conveyancer can become expensive if the sale stalls through slow replies.

Landlords selling with tenants in situ should speak to property sales support and legal and financial property advice before deciding whether to sell vacant or tenanted.

EPC, mortgage charges and preparation costs

An EPC is a small cost but it is not optional for most sales. Check whether a valid certificate exists before paying for a new one. If it has expired, order a new one before the property is launched.

Mortgage charges can be the painful line. A small exit fee is one thing; a 2% or 3% early repayment charge on a large mortgage can outweigh the agent and legal fees. Ask for a redemption statement before listing.

Preparation should protect the price, not satisfy personal taste. Deep cleaning, garden clearance, small repairs and clear paperwork often produce better value than expensive cosmetic works a buyer may replace anyway.

Capital Gains Tax for buy-to-let and second homes

Most people do not pay Capital Gains Tax when selling their only or main home if Private Residence Relief applies. Buy-to-let properties, second homes, inherited properties and mixed-use cases can be different.

GOV.UK says CGT may apply when selling property that is not your home, such as buy-to-let property, and most UK property disposals must be reported and paid within 60 days if tax is due. From 6 April 2026, higher and additional rate taxpayers pay 24% on gains, while basic-rate taxpayers may pay 18% or 24% depending on income and gain.

Keep purchase records, legal fees, stamp duty records, improvement invoices, selling fees and valuation evidence. Speak to an accountant before exchange, not after completion.

A £450,000 London sale example

On a £450,000 sale, a 1.2% agent fee plus VAT is £6,480. Add leasehold conveyancing at around £1,400, a £350 management pack, £100 EPC, £1,200 preparation, £1,500 removals and £150 lender admin, and the subtotal reaches £11,180 before early repayment charge or tax.

If there is a 2% early repayment charge on a £230,000 mortgage, that adds £4,600. If it is a buy-to-let with a taxable gain, the final sale cost can be much higher. This is why selling decisions need a net proceeds calculation.

Does selling make more sense than keeping the rental property?

For landlords, selling is not just a disposal. It is the end of a future income stream. If the property is failing because of poor management rather than weak fundamentals, sale may not be the only route.

Compare sale proceeds with portfolio review for landlords, AMS guaranteed rent service and free rental valuation before committing.

How to reduce cost without weakening the sale

Reducing sale cost does not mean choosing the cheapest option at every line. It means cutting waste while protecting the final price and the chance of completion. A cheap agent who fails to progress the sale can cost more than a better agent charging a higher fee.

Get more than one valuation, negotiate the fee, check VAT, order leasehold packs early, instruct a conveyancer who understands the property type and fix obvious defects before photography. Avoid overpricing. A stale listing often costs more than a realistic launch price.

If the property is tenanted, prepare the tenancy file before marketing. Missing deposit, gas, electrical or licence evidence can slow an investor sale or create buyer nervousness.

Leasehold and landlord sales need extra preparation

A leasehold sale often needs a management pack, ground rent and service charge statements, building insurance evidence, major works information and replies from the freeholder or managing agent. Those documents can be slow and expensive.

A landlord sale adds rent schedule, tenancy agreement, deposit evidence, safety certificates, inventory, repair records and confirmation of whether the buyer is taking tenants in situ or requiring vacant possession.

Preparing these documents before launch reduces the chance of losing a buyer after offer. The cheapest sale is the one that reaches exchange cleanly.

How AMS frames the sell-or-keep decision

A landlord sale should be tested against three figures: net cash after sale, expected open-market net rental income and fixed income under guaranteed rent. The sale route may still be right, but the decision should not be made only because one tenancy went badly.

If the property is structurally weak, heavily mortgaged, facing large works or producing poor yield, sale may be sensible. If the property is in a strong rental location but has suffered from weak management, better management or guaranteed rent may solve the problem without triggering sale costs and possible tax.

The point is to avoid an emotional disposal. Landlords should know what they will receive after agent fees, conveyancing, mortgage redemption, early repayment charges, repairs and tax before they give up future rent.

The seller file that avoids late price chips

A buyer usually negotiates hardest when they discover uncertainty late. Build the seller file before launch: title information, lease pack request, EPC, certificates, planning or building-control documents, guarantees, service charge records, tenancy papers where relevant and a clear list of known works.

This reduces the chance of a buyer lowering the offer after survey or conveyancing. It also helps the estate agent answer sensible questions quickly instead of losing momentum while documents are chased.

For a landlord sale, the seller file should also include rent statements, deposit protection evidence, inventory and repair records. Investor buyers price risk aggressively when the tenancy file is thin.

Why one extra month on the market has a cost

A slow sale is not free. Another month on the market can mean another mortgage payment, another service charge demand, another council tax period if the property is empty, another insurance month and more risk that the listing begins to look stale.

That is why pricing, paperwork and presentation are part of the selling cost. They may not appear as invoices, but they decide how long the property sits unsold.

Example £450,000 sale

| Cost | Estimated amount |

| Agent fee at 1.2% + VAT | £6,480 |

| Leasehold conveyancing | £1,400 |

| Leasehold management pack | £350 |

| EPC | £100 |

| Repairs and preparation | £1,200 |

| Removals | £1,500 |

| Subtotal before ERC/CGT | £11,030-£11,180 approx. |

FAQs

What is the average cost of selling a house?

Many sellers should budget around £5,000 to £15,000 before early repayment charges, major repairs or tax.

Do sellers pay stamp duty?

No. Stamp Duty Land Tax is normally a buyer cost in England and Northern Ireland.

Do I need an EPC to sell?

In most cases yes. It must be ordered before marketing if a valid certificate is not already available.

Do landlords pay CGT when selling?

They may if the property is a buy-to-let, second home or otherwise not fully covered by Private Residence Relief.

Should landlords sell with tenants in situ?

It depends on buyer demand, tenancy records, rent level, tax, timescale and whether vacant possession is needed.

Speak to AMS before you commit

If this decision affects rent, compliance, sale timing or tenant risk, speak to AMS Housing Group before committing. AMS is based at 29 Longbridge Road, Barking IG11 8TN and works across all 33 London boroughs and Essex. Call 020 3793 2247 or use the valuation enquiry route to compare the numbers for your own property.