Key takeaways

- Keep rental income, personal spending and deposits separate.

- Track allowable expenses with invoices, dates and property references.

- Repairs and improvements can be treated differently for tax, so do not guess.

- Section 24 means mortgage interest is not deducted in the old way for individual landlords.

- Quarterly reviews help landlords make decisions before the tax year becomes messy.

Rental property accounting is not just a year-end tax job. It is the system that tells a landlord whether the property is working, which costs are rising and whether management, sale or guaranteed rent should be considered.

This guide explains rental property accounting in the UK for landlords in 2026, including income records, expenses, repairs versus improvements, mortgage interest, Section 24 and quarterly review habits. It is general guidance only; landlords should use a qualified accountant for tax advice.

Set up records before the tax year gets messy

The best accounting system is simple enough to keep up to date. Each property should have records for rent due, rent received, arrears, deposit, repairs, insurance, certificates, mortgage interest, service charges, licence costs, agent fees and professional fees. If the landlord owns more than one property, each property needs its own ledger.

A separate bank account is not legally required in every case, but it makes life easier. Mixing personal spending and rental costs creates confusion and makes it harder to answer HMRC, an accountant or a buyer. Clear records also help when comparing whether to keep, sell or move to guaranteed rent.

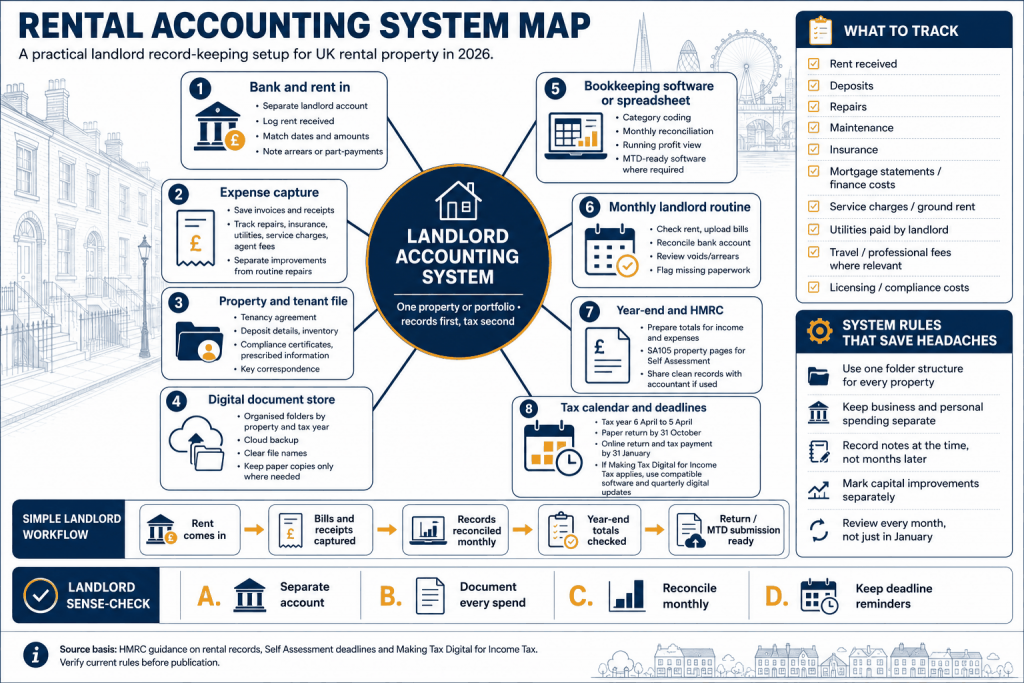

The rental-accounting-system-map image should sit here because it shows the practical file structure: income, expenses, tax, mortgage, compliance, deposits and quarterly review.

Separate income, expenses and deposits

Rent received is income. A tenant deposit is not landlord income when it is properly protected; it is money held under deposit rules. Arrears should be recorded separately from rent received so the landlord can see what is due, what has been paid and what needs action.

Expenses should be recorded with receipts, invoices and bank references. Useful categories include repairs, maintenance, insurance, agent fees, compliance certificates, licence fees, accountancy, legal costs, service charges and mortgage interest. The category matters because not every payment is treated the same for tax.

A landlord who cannot separate rent, deposit and expenses will struggle to make good decisions, even if they file a return on time.

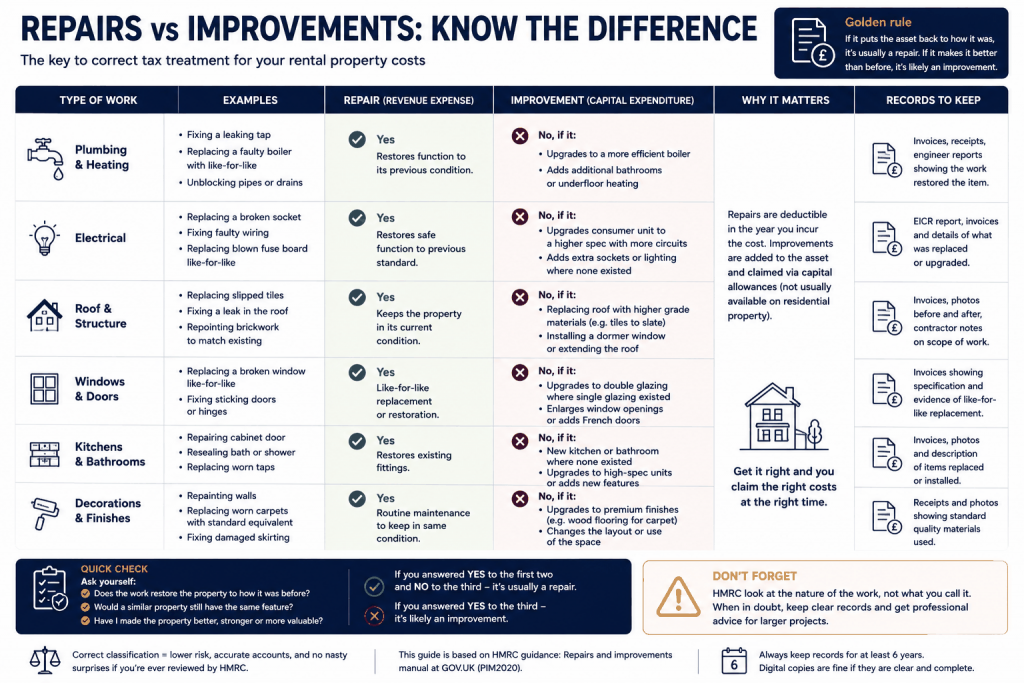

Repairs versus improvements

Repairs and improvements need careful handling. Repairing a broken boiler, replacing like-for-like fittings or fixing damage may be different from improving the property beyond its previous standard. The tax treatment can vary, so landlords should keep descriptions, invoices and before-and-after notes rather than rely on memory.

This is not just an accountant’s problem. If the landlord later sells the property, capital works may affect Capital Gains Tax calculations. If the landlord wants a valuation, clear records help explain whether recent spending improved the asset or just kept it lettable.

The repairs-vs-improvements image belongs here because it gives landlords a decision table they can use before coding expenses.

Mortgage interest, Section 24 and cash flow

Individual landlords should understand that mortgage interest is not deducted in the old way. Section 24 restricts finance cost relief, which can make the tax bill feel high compared with cash profit. This is one of the main reasons landlords with mortgages need proper forecasts rather than a simple rent-minus-mortgage view.

Salary also matters because rental profit is added to other income and taxed at the landlord’s marginal rate. A property that looks profitable before tax may create a difficult cash-flow position for a higher-rate taxpayer. An accountant should be involved where finance, company structures or multiple properties are involved.

AMS does not replace tax advice, but clean accounting records make it easier for landlords and accountants to make sensible decisions.

What landlords should review every quarter

A quarterly review should answer six questions: has rent been paid, what arrears exist, what repairs are outstanding, what certificates expire soon, what tax reserve is building, and does the annual net return still justify the route? This is much more useful than waiting until January with a box of receipts.

The quarterly-review checklist image belongs here because it gives landlords a repeatable routine: rent ledger, arrears, repairs, certificates, tax reserve, mortgage interest, insurance and portfolio decision.

Quarterly reviews also reveal when the problem is not tax but management. Rising repairs, repeated arrears or high voids may point to the need for full management, guaranteed rent or sale.

Making Tax Digital and digital records

Landlords should prepare for digital record keeping even if they are below the threshold today. Making Tax Digital for Income Tax Self Assessment is being phased in by income level, and landlords with larger rental income need to be ready for digital records and more regular submissions. Even where the rules do not yet apply, digital records make decisions easier.

The key is not expensive software. The key is consistent categories, attached invoices, rent records, deposit notes and quarterly review. A spreadsheet can work for a small landlord if it is maintained. Larger portfolios usually need software and accountant oversight.

Property-level profit and loss

A portfolio landlord should not look only at total rental profit. Each property needs its own profit and loss view. One high-performing property can hide another that is losing money after repairs, voids and finance costs. That matters when deciding whether to sell, refinance or move one asset into guaranteed rent.

Property-level accounting should include rent, arrears, service charge, insurance, finance costs, maintenance, certificates, licence costs, management fees and tax reserve. Once those numbers are visible, the landlord can make a decision based on evidence rather than habit.

Accounting records as management evidence

Accounting records also support management. A rent ledger helps with arrears action. Repair invoices support compliance. Deposit records protect against disputes. Insurance and certificate costs show whether the property is properly maintained. The same records used for tax can therefore protect the landlord in a tenant complaint or sale due diligence.

AMS encourages landlords to connect accounting, compliance and inspections because the property does not operate in separate boxes. The best decisions come from one clean view of rent, risk, condition and future plans.

London accounting checks that affect portfolio decisions

London rental accounting should show property-level performance. A landlord with several homes should know which property is producing cash, which is being carried by the others and which one needs a rent review, repair plan, refinance or sale discussion.

The records should also separate tax profit from cash flow. Mortgage interest restrictions, capital repayments, repairs, improvements and service charges can make the tax result look different from the landlord’s bank balance.

When the accounting file is clean, AMS can compare management routes more fairly. The numbers show whether the landlord needs higher rent, lower risk, better repairs control, fixed income or a portfolio restructure.

Final accounting check before year-end

Before year-end, landlords should reconcile rent due against rent received, chase missing invoices, separate capital works from repairs, confirm mortgage interest totals and check whether any deposit deductions, insurance claims or legal costs need separate treatment. This review should happen before the accountant asks for records, not after the deadline pressure starts. It gives the landlord time to correct gaps and understand the property result.

Accounting support for better landlord decisions

Good accounting is not just compliance. It shows whether a property is worth keeping. A landlord can compare self-management, agent management, guaranteed rent and sale only when rent, costs and tax are visible. Without records, the decision becomes guesswork.

Frequently asked questions

Do landlords pay tax on rent or profit?

Landlords are generally taxed on rental profit, but mortgage interest restrictions can affect the result for individual landlords.

Should deposits go through the landlord accounts?

They should be recorded clearly, but protected deposits are not treated like rental income.

How often should landlords review accounts?

Quarterly reviews are useful because they catch arrears, repairs, expiring certificates and tax reserves before year-end.