Table of contents

Table of Contents

Key Takeaways

- Right to Buy Sales Increasing: 7,494 sales in 2024-25, a 7% increase, but still far from historic highs.

- Massive Discount Reductions: From November 2024, maximum discounts were slashed from £102k-£136k to just £16k-£38k depending on region.

- Future Restrictions Likely: The Labour government plans to increase the qualifying period to 10 years and reduce initial discounts to 5%.

- Mortgage Market Adapting: Over 40 lenders still offer Right to Buy mortgages, with some offering 100% of the discounted price.

- Hidden Costs: Service charges (£1.2k-£3k annually), major works (£10k+), and lease extensions (£5k-£15k+) are significant risks.

- AMS Housing Group as an Alternative: For landlords, our guaranteed rent scheme offers a secure income without the complexities of buying or managing ex-council properties.

Introduction: The Changing Landscape of Right to Buy

The Right to Buy scheme, a cornerstone of UK housing policy since 1980, has enabled over 2 million council tenants to purchase their homes at a discount. However, the landscape is shifting dramatically. With significant discount reductions in late 2024 and further restrictions on the horizon, is buying a council house still a viable option in 2025? This comprehensive guide will walk you through the new rules, the financial implications, and whether this long-standing scheme still holds value for aspiring homeowners.

Understanding the Right to Buy Scheme

The Right to Buy scheme gives eligible council and housing association tenants the legal right to buy the home they live in at a discounted price. The scheme was introduced to promote homeownership and has been a popular route onto the property ladder for millions.

Who is Eligible for Right to Buy?

To be eligible for the Right to Buy scheme, you must meet the following criteria:

- Public Sector Tenant: You must be a secure tenant of a public sector landlord, such as a council, housing association, or NHS trust.

- Tenancy Period: You must have been a public sector tenant for at least 3 years (this does not have to be continuous).

- No Legal Issues: You must not have any outstanding possession orders against you.

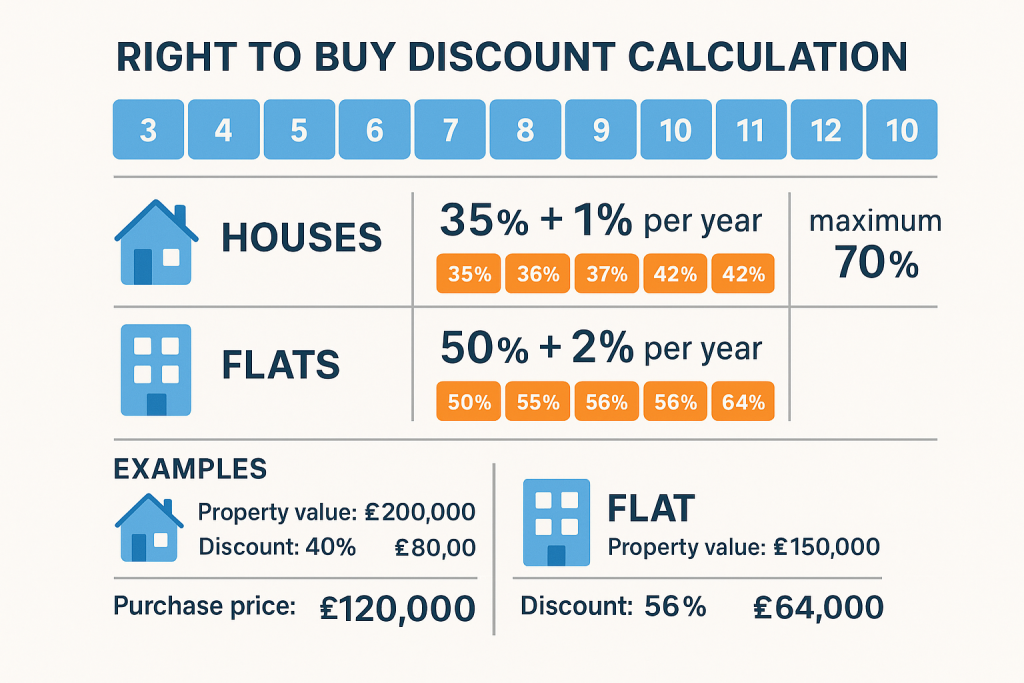

The Right to Buy Discount: How it Works

The discount you receive is based on the type of property, how long you have been a tenant, and the region you live in.

- Houses: The discount starts at 35% for 3-5 years of tenancy, increasing by 1% for each additional year, up to a maximum of 70%.

- Flats: The discount starts at 50% for 3-5 years of tenancy, increasing by 2% for each additional year, up to a maximum of 70%.

However, the most significant change is the reduction in the maximum cash discount, which severely limits the benefit for many tenants.

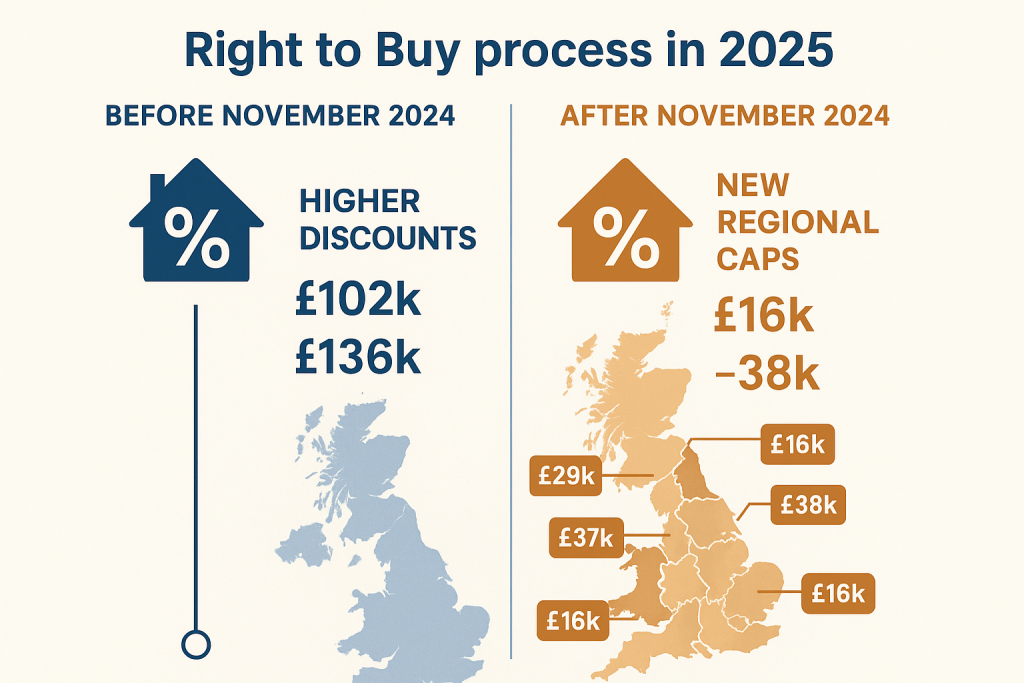

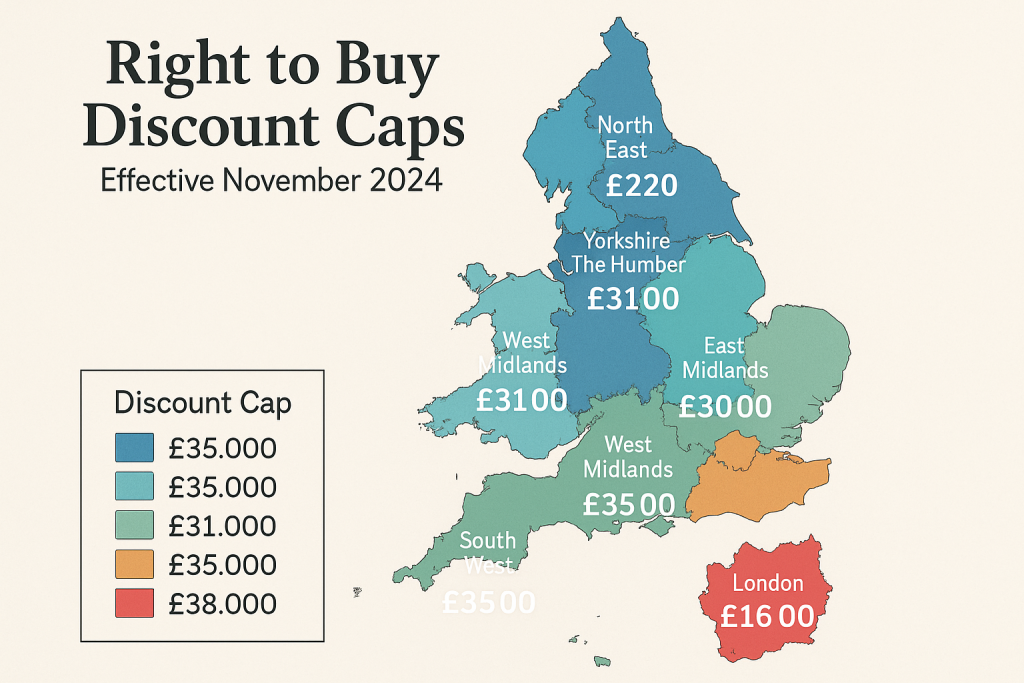

The New Rules: November 2024 Discount Reductions

In a move to preserve social housing stock, the government drastically reduced the maximum Right to Buy discounts from November 21, 2024.

| Region | New Maximum Discount |

|---|---|

| North East | £22,000 |

| North West | £26,000 |

| Yorkshire and the Humber | £24,000 |

| East Midlands | £24,000 |

| West Midlands | £26,000 |

| Eastern | £34,000 |

| South East | £38,000 |

| South West | £30,000 |

| London | £16,000 |

This is a substantial reduction from the previous caps of £102,400 in England and £136,400 in London. For many, this change has made the Right to Buy scheme significantly less attractive.

The Application Process: A Step-by-Step Guide

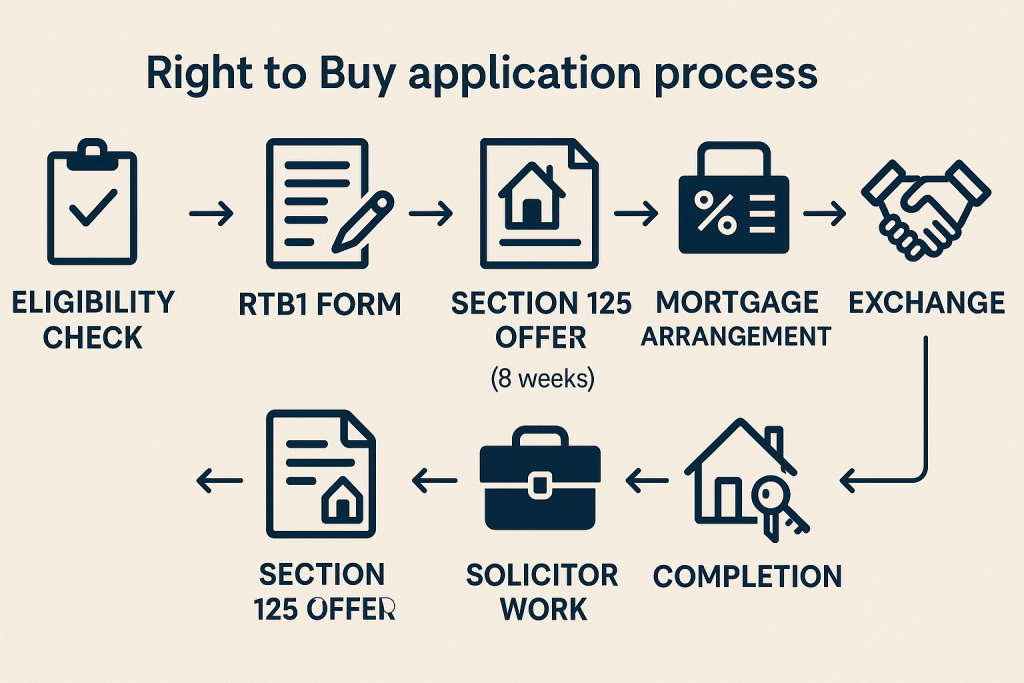

Navigating the Right to Buy process can be complex. Here is a simplified timeline of what to expect:

- Eligibility Check: Ensure you meet all the criteria before applying.

- RTB1 Form: Complete and submit the Right to Buy application form to your landlord.

- Landlord’s Response: Your landlord has 4 weeks to respond, confirming or denying your right to buy.

- Section 125 Offer: If eligible, your landlord must send you a Section 125 offer notice within 8 weeks (for freehold) or 12 weeks (for leasehold). This will include the property valuation and your discount.

- Mortgage Arrangement: This is the time to secure a mortgage. Many lenders offer specialist Right to Buy mortgages.

- Solicitor Work: Instruct a solicitor to handle the legal aspects of the purchase.

- Exchange and Completion: Once all legal work is complete, you will exchange contracts and complete the purchase.

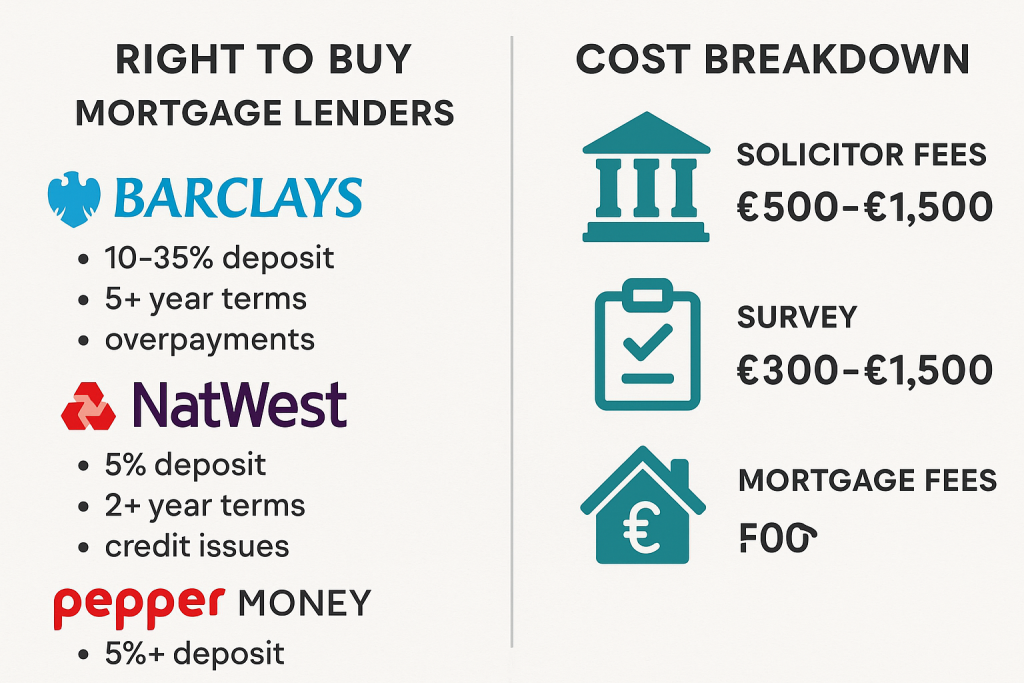

Financing Your Right to Buy Purchase

Securing a mortgage for a Right to Buy property is a crucial step. The good news is that many lenders are still active in this market.

Key Lenders and Products

- Barclays: Offers a zero-deposit mortgage, using the Right to Buy discount as the deposit.

- NatWest: Lends up to 100% of the discounted purchase price.

- Pepper Money: A specialist lender for those with adverse credit history.

- Leeds Building Society: Offers competitive fixed-rate mortgages for Right to Buy.

The Hidden Costs of Buying a Council Property

While the discount can be appealing, there are significant hidden costs to consider, especially for leasehold properties (flats and maisonettes).

- Service Charges: These can range from £1,200 to £3,000 per year and cover the upkeep of communal areas.

- Major Works: You will be liable for your share of major works, such as roof repairs or lift replacements, which can cost over £10,000.

- Lease Extensions: If the lease has less than 80 years remaining, it can be expensive to extend, costing £5,000 to £15,000 or more.

- Landlord Insurance: You will need to arrange your own buildings insurance.

The Future of Right to Buy: Further Restrictions Ahead

The Labour government has announced plans for further restrictions on the Right to Buy scheme, aiming to protect social housing stock.

- Increased Qualifying Period: The minimum tenancy period is set to increase from 3 to 10 years.

- Reduced Initial Discounts: The starting discount will be lowered to just 5%.

- New Build Exemption: Newly built social housing will be exempt from Right to Buy for 35 years.

These changes signal a clear direction of travel: the Right to Buy scheme is becoming less generous and more restrictive.

Is Buying a Council House Still a Good Idea in 2025?

With reduced discounts, the prospect of further restrictions, and the significant hidden costs of leasehold properties, the Right to Buy scheme is no longer the straightforward path to homeownership it once was. For many, the financial benefits have been severely eroded.

An Alternative for Landlords: Guaranteed Rent

For property owners and landlords, the complexities and risks of the rental market are ever-increasing, from the abolition of Section 21 to rising landlord costs. Instead of navigating the challenges of buying and letting an ex-council property, our guaranteed rent scheme offers a hassle-free alternative.

- Guaranteed Monthly Income: We pay you a fixed rent every month, regardless of whether the property is occupied.

- No Voids or Arrears: We eliminate the risk of void periods and rent arrears.

- Full Property Management: We handle all aspects of tenant management, maintenance, and compliance.

Conclusion: A New Era for Council Tenants and Landlords

The Right to Buy scheme is at a crossroads. While it may still offer a route to homeownership for some, the significant changes in 2024 and the prospect of further restrictions mean that it is no longer the attractive proposition it once was. For landlords, the complexities of the rental market make our guaranteed rent scheme a compelling alternative, offering financial security without the stress of property management.

If you are considering your options, whether as a tenant or a landlord, it is essential to seek professional advice. Contact us today for a free, no-obligation portfolio review to see how we can help you achieve your property goals.

References

- GOV.UK. (2025, August 21). Right to Buy sales and replacements, England: April 2024 to March 2025. Retrieved from https://www.gov.uk/government/statistics/right-to-buy-sales-and-replacements-england-2024-to-2025/right-to-buy-sales-and-replacements-england-april-2024-to-march-2025

- Pennington Solicitors. (2024, November 4). Right to Buy: changes announced in October 2024 Budget. Retrieved from https://www.penningtonslaw.com/news-publications/latest-news/2024/right-to-buy-changes-announced-in-october-2024-budget

- GOV.UK. (2025, July 2). Government response to the consultation on Reforming the Right to Buy. Retrieved from https://www.gov.uk/government/consultations/reforming-the-right-to-buy/outcome/government-response-to-the-consultation-on-reforming-the-right-to-buy

- Forbes Solicitors. (2024, November 12). Government announces reduction in Right to Buy Discounts from 21st November 2024. Retrieved from https://www.forbessolicitors.co.uk/articles/government-announces-reduction-in-right-to-buy-discounts-from-21st-november-2024

- Barclays. (2025, April 1). Barclays offers zero deposit mortgage for Right to Buy applicants. Retrieved from https://home.barclays/news/press-releases/2025/04/barclays-offers-zero-deposit-mortgage-for-right-to-buy-applicant/

- NatWest Intermediaries. (2025). Lending Criteria. Retrieved from https://www.intermediary.natwest.com/intermediary-solutions/lending-criteria.html

- Pepper Money. (2025). Right to Buy Mortgage Products. Retrieved from https://www.pepper.money/broker/mortgage-products/right-to-buy-mortgage-products/

- Leeds Building Society. (2025). Right to Buy Mortgage Range. Retrieved from https://www.leedsbuildingsociety.co.uk/mortgages/right-to-buy-mortgages/

- BBC News. (2025, September 18). Labour plans further Right to Buy restrictions in England. Retrieved from https://www.bbc.com/news/articles/c6257pr3q76o

- Uswitch. (2025). Right To Buy Mortgages 2025. Retrieved from https://www.uswitch.com/mortgages/guides/right-to-buy/