Key takeaways

- Solicitor fees are only one part of the cost; tax, SDLT, CGT, mortgage consent and administration can matter more.

- Different trusts are taxed differently, so “putting a house in trust” is not one simple product.

- Rental property creates extra issues because income, repairs, licences and management responsibility must still be handled.

- Landlords should speak to a solicitor and tax adviser before transferring property.

Putting a house into trust is a legal and tax decision, not a shortcut. The cost can include professional advice, trust drafting, Land Registry work, SDLT, capital gains tax, inheritance tax exposure and ongoing administration.

For landlords, there is another layer: the property may still need to be let, managed, insured, licensed and repaired. A trust does not remove those duties.

AMS Housing Group was founded in 2010, manages 500+ properties across all 33 London boroughs and Essex, and works from 29 Longbridge Road, Barking IG11 8TN. This article is written for practical landlord decision-making, not as legal, tax, mortgage or insurance advice. Where your decision affects tax, lending, eviction, trust planning or litigation, speak to a qualified professional before acting.

The cost range is only the start

A simple will trust or bare trust may cost far less than a complex lifetime discretionary trust, but the setup bill is not the full decision. The tax position can outweigh the solicitor fee.

GOV.UK explains that trusts are used to manage assets for beneficiaries and that different trusts are taxed differently. That is why a landlord should not choose a trust from a headline price.

The first existing image belongs here as a trust cost stack: advice, drafting, registration, SDLT, CGT, IHT, lender consent and annual administration.

Related AMS route: legal and financial property advice.

The tax questions that matter more than the solicitor fee

Ask whether the transfer triggers Stamp Duty Land Tax, capital gains tax or inheritance tax consequences. If the property has a mortgage, taking on debt or transferring beneficial ownership can change the SDLT analysis.

A trust can also affect the residence nil-rate band, ten-year charges, income-tax treatment and future sale planning. These are specialist questions, not content-marketing answers.

This article gives general guidance only. For any trust involving a house, particularly a rental property, the landlord needs qualified legal and tax advice.

Related AMS route: portfolio review for landlords.

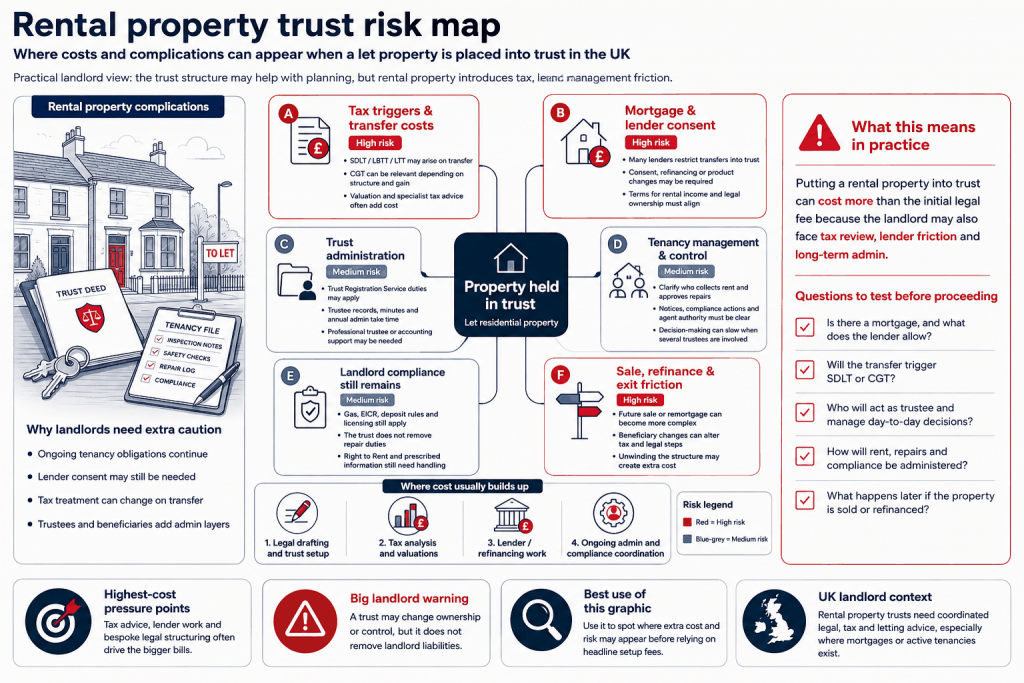

Rental property complications inside a trust

Rental property still has rent collection, repairs, insurance, licences, tax returns and tenant communication. The trust deed must make clear who has authority to make decisions and how income is handled.

The second existing image should be used here as a rental property trust risk map. It should connect trustees, beneficiaries, mortgage lender, insurer, tenant, managing agent and HMRC.

If a trustee is slow to approve repairs or unclear about authority, the tenant does not care that the asset sits in a trust. The legal structure can create practical delay if it is poorly planned.

Related AMS route: full property management in London.

Mortgage, insurance and leasehold consent

A mortgaged property cannot be moved into trust without considering lender consent. The mortgage terms may prohibit transfer, treat it as a disposal or require a new lending decision.

Insurance must also match the ownership and occupation position. A rental property owned by trustees but insured as a simple owner-occupied home can create problems if there is a claim.

Leasehold flats need extra care. The lease may require notices, consents or registration of transfer. Service charges and major works remain a practical cost.

Related AMS route: property sales support.

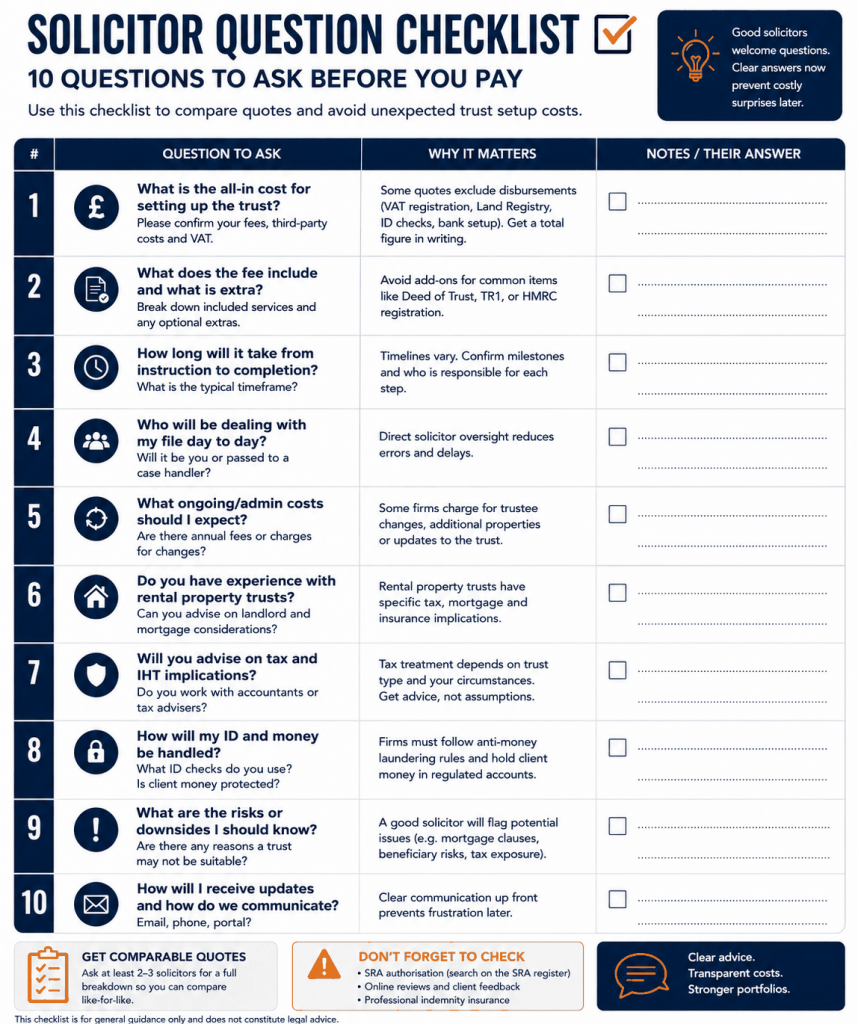

What to ask a solicitor before paying

The third existing image belongs after a solicitor question checklist. The questions should cover trust type, tax, SDLT, CGT, IHT, mortgage consent, trustee powers, rent handling, sale process and exit options.

Ask for a written scope before paying. A cheap quote that only drafts a deed may not include tax advice, registration, lender correspondence or advice on rental income.

Landlords should also ask whether a trust is actually the right tool. A will, declaration of trust, company structure, sale, insurance policy or estate-planning advice may be more suitable depending on the goal.

Related AMS route: contact AMS.

The ongoing administration cost landlords forget

Trusts can need annual tax returns, trustee decisions, accounts, beneficiary records, registration updates and professional advice. The first-year solicitor bill is not the end of the cost.

If the trust receives rental income, the trustees need a process for rent collection, repairs, expenses and tax reporting. That can be simple for one property or complicated where there are multiple beneficiaries and competing interests.

A landlord should ask who will make quick decisions if the tenant reports a leak, the insurer asks for paperwork or the council requests a licence document.

When selling may be cleaner than using a trust

Sometimes the goal behind a trust is asset protection, inheritance planning or family fairness. Sometimes the cleaner answer is a sale, a will update, life insurance, a declaration of trust or a different ownership structure.

For landlords with low-yielding properties, high repair exposure or unresolved leasehold issues, putting the property into trust can preserve a problem rather than solve it. The property should be reviewed commercially before legal structuring.

AMS property sales and portfolio review support can help landlords understand whether the property is worth retaining before they pay for complex planning.

Trust planning should start with the property file

A solicitor will give better advice if the landlord can produce the title, lease, mortgage statement, insurance schedule, tenancy details, rent accounts and repair history. A trust structure built without those documents is only half a plan.

For rental property, trustee decision-making must be practical. Someone must be able to approve repairs, sign management agreements, deal with insurance and respond to tenants without waiting weeks for a family discussion.

London landlord angle: high values make mistakes expensive

London property values can push ordinary family planning into serious tax and legal territory. A small percentage mistake on a high-value home can cost more than several years of professional advice.

That is why landlords should not move property into trust from a template or a general article. The property value, mortgage, ownership history, beneficiaries and rental plan all need professional review.

Before transferring the property

Do not transfer the property until the tax, mortgage, insurance and management position have been checked together. A trust that works for inheritance planning can still create rental or lending problems if planned badly.

Put the advice in writing. Trust decisions often affect other family members years later, so the reason for the structure should be recorded while everyone still remembers it clearly.

This is especially important with rental property because trustees, beneficiaries and managing agents may all need to understand who can approve repairs, collect rent, sign documents and sell the asset later.

Mini example: the cheap trust that becomes expensive

A landlord may receive a quote of £1,500 for trust paperwork and assume the problem is solved. But if the property has a mortgage, a gain since purchase, rental income and several intended beneficiaries, the professional fee is only the first question.

The plan may need lender consent, tax advice, trustee registration, Land Registry work, ongoing accounts and a decision about how repairs and rent will be managed. Those costs and responsibilities can be larger than the first quote.

A trust should therefore be priced as a legal structure over time, not as a document bought once.

Information to prepare before professional advice

Before meeting a solicitor, gather the title, mortgage statement, lease, property value, purchase history, ownership shares, rental income, beneficiaries, existing will and the reason for considering a trust. Better information leads to better advice.

Write down the real objective. Is the landlord trying to reduce inheritance tax, protect a vulnerable beneficiary, pass wealth to children, manage a blended family or avoid probate? Different goals point to different tools.

Do not hide mortgage or rental issues from the adviser. A trust plan that ignores the lender, insurer, tenant or HMRC will not be safe in practice.

Final trust-planning check before publication

The reader should not leave thinking a trust is a cheap tax shortcut. A trust is a legal structure with duties, tax treatment and management consequences, especially when the asset is a rental property.

Frequently asked questions

Can I put my house in trust to avoid inheritance tax?

A trust may have inheritance tax consequences, but it is not a simple avoidance tool. Take specialist advice before transferring property.

Does putting a house in trust trigger Stamp Duty?

It can, depending on the trust type, consideration and debt position. Check SDLT advice before transfer.

Can a mortgaged house go into trust?

Only with careful lender and legal advice. Mortgage terms may restrict or prevent transfer.

Is a trust suitable for rental property?

Sometimes, rental income, repairs, tax and trustee authority must be planned properly.

What landlords should do next

Treat the trust fee as the first invoice, not the whole cost. Get legal and tax advice before moving any rental property into trust.

For a property-specific view, request a free valuation from AMS Housing Group, or call 020 3793 2247. AMS is based at 29 Longbridge Road, Barking IG11 8TN and works across all 33 London boroughs and Essex.