Key takeaways

- Guaranteed rent normally pays less than open-market rent each month, but removes many costs and risks from the landlord side.

- The fair comparison is annual net income, not monthly gross rent.

- The model is strongest for landlords who value certainty, have limited time, or have suffered voids, arrears or management stress.

- It is not ideal if the landlord wants full control, plans to sell immediately, or has a property unsuitable for provider management.

Guaranteed rent is worth it only when the lower monthly figure produces a stronger annual result or a cleaner risk position. The question is not whether the market rent is higher. It usually is. The question is how much of that rent the landlord keeps after fees, voids, repairs, arrears and time.

This guide gives London landlords a practical way to judge guaranteed rent in 2026. It uses AMS’s fixed-income model as a comparison point, but it also explains when traditional letting or full management may be the better fit.

The honest trade-off: lower headline rent, steadier income

Guaranteed rent begins with an exchange. The landlord accepts a fixed rent below the open-market figure. In return, the provider takes on void risk, tenant-management pressure and a large part of the operational workload. That is why a guaranteed rent offer should not be judged as a discount alone. It should be judged as a risk transfer.

For example, a Barking flat at an open-market rent of £1,500 pcm may attract a guaranteed rent offer around 85-92% of that figure. On the surface, the landlord gives up money. Over a year, however, one void month, an agent fee, a failed tenancy or a legal problem can remove more than the monthly gap.

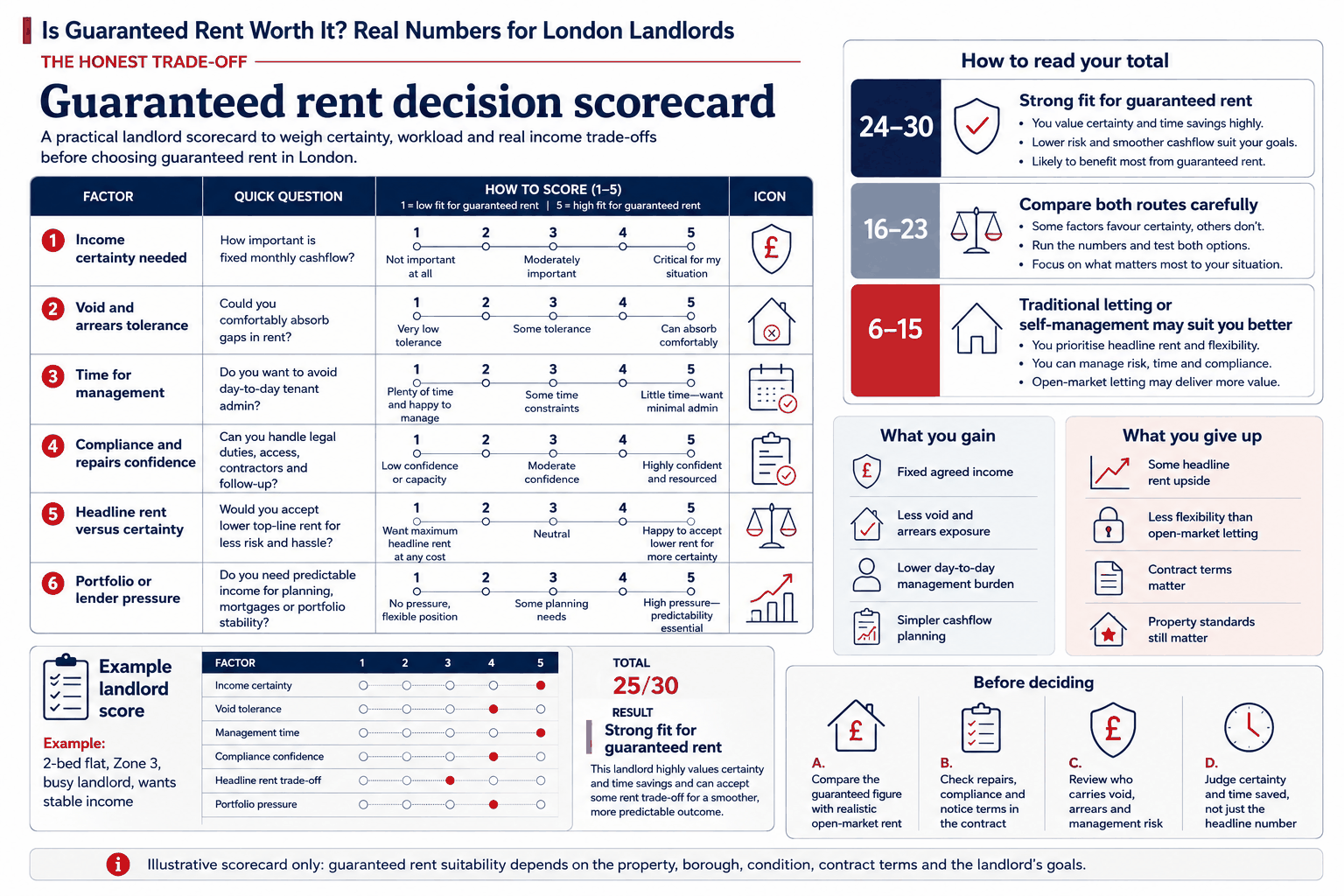

The decision-scorecard image belongs here. It should show income certainty, time, repairs, voids, arrears, control and contract length as separate scoring factors.

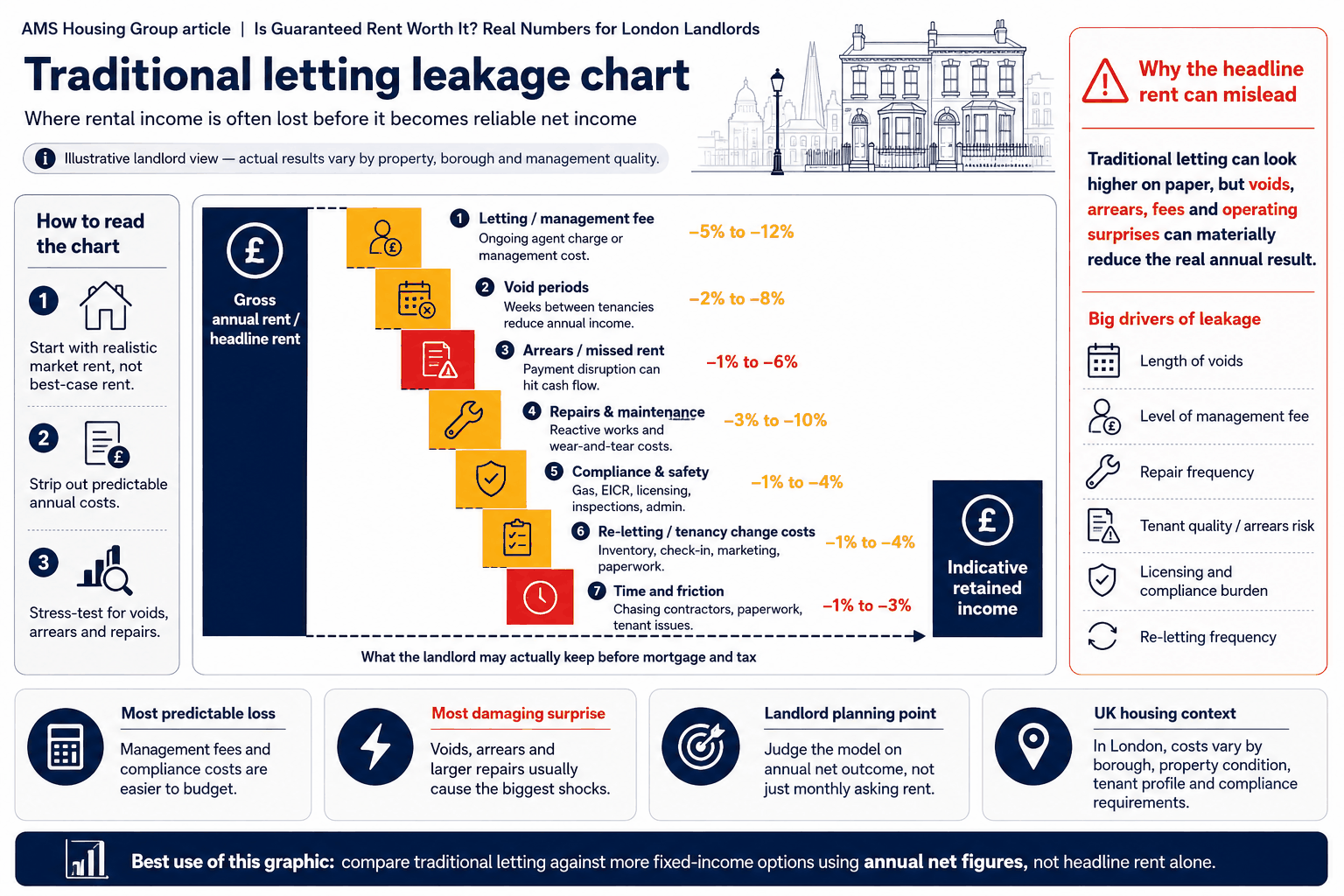

Where traditional letting leaks profit

Traditional letting can work very well when demand is strong, the tenant is stable and the landlord has a good agent. The weak point is that the risk stays with the landlord. A void between tenants, a boiler issue, tenant-find fee, renewal fee, management percentage, check-out cost or arrears case all come out of the landlord’s return.

London landlords often overestimate the value of the highest asking rent and underestimate the cost of getting to that number. A six-week void at £1,800 pcm is not a small inconvenience; it is more than £2,400 lost before repairs or re-marketing costs are counted. The landlord also carries the stress of decisions and disputes.

The leakage chart sits naturally here because it explains how gross rent is reduced by real costs before the landlord sees the annual result.

Which landlords benefit most from guaranteed rent

Guaranteed rent is usually strongest for landlords who want regular income without managing day-to-day issues. That includes overseas landlords, portfolio owners, busy professionals, landlords tired of arrears, and owners of properties where a stable fixed figure is more useful than chasing the highest possible rent.

It can also help after the 2026 tenancy reforms because possession risk is more evidence-led and slower when management is weak. A landlord who has no time to document repairs, monitor arrears and manage compliance may find that the fixed monthly figure is worth the trade-off.

The model is not a shortcut around landlord law. A serious provider still needs a compliant property, sensible rent and a clear contract. If someone offers above market rent with vague terms, that is not a better guaranteed rent deal. It is a warning sign.

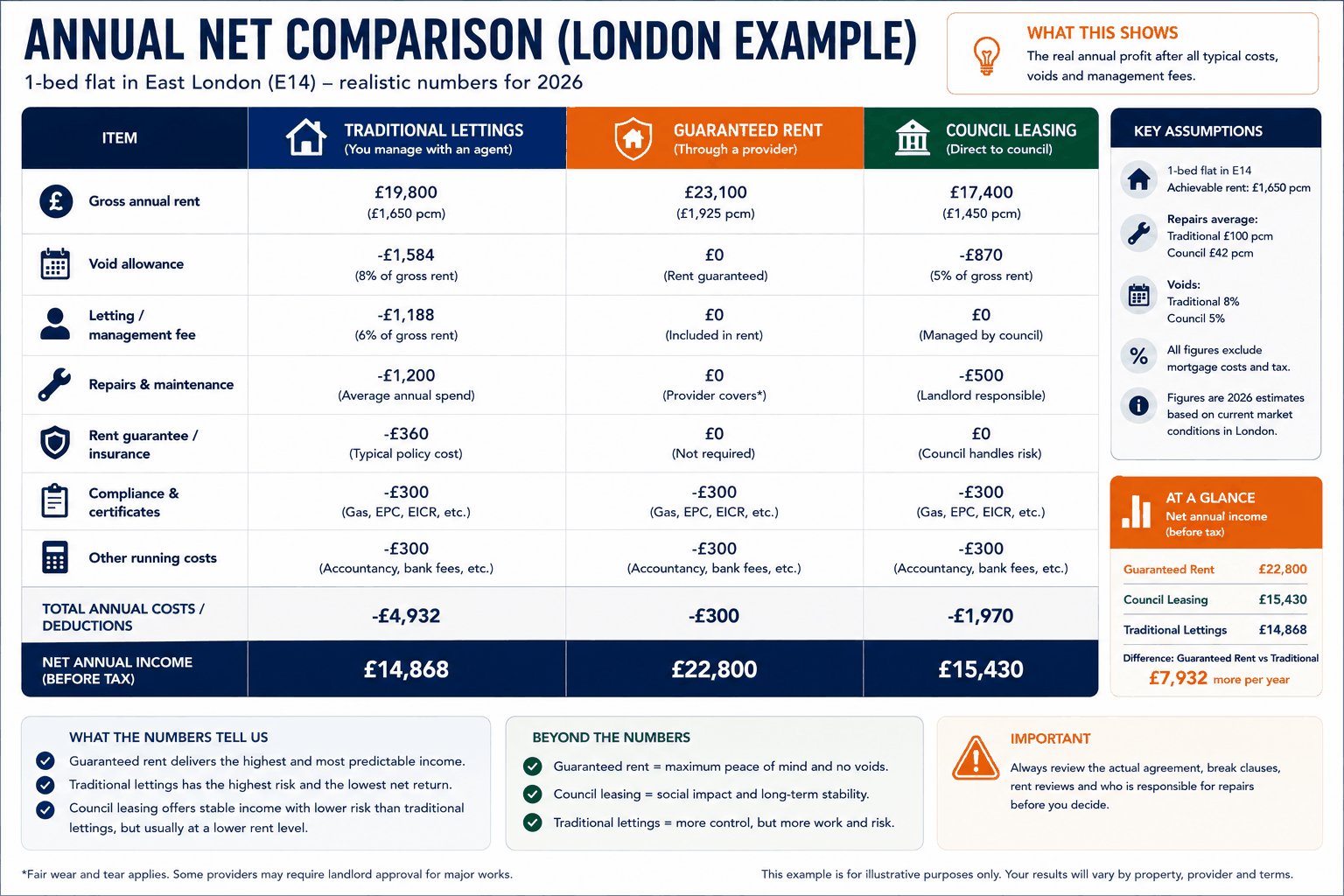

A realistic annual net comparison

The useful comparison is simple. Start with market rent for 12 months, then subtract realistic costs: agent management, tenant-find, voids, inspections, certificates, repairs, arrears risk, legal time and landlord time. Then compare that with the guaranteed rent total for the same period.

For a landlord who lives near the property and has reliable tenants, traditional letting may still produce a higher net result. For a landlord who has one difficult tenancy every few years, lives abroad, or wants fixed income to match a mortgage or family budget, guaranteed rent can produce a better practical result even with a lower monthly figure.

The annual-net-comparison image belongs here. It should not just show rent. It should show rent after deductions, so the landlord sees the real trade-off.

Questions to ask before accepting a guaranteed rent offer

Ask how the offer was calculated, what rent evidence was used, who pays for repairs, how inspections work, what happens at handback, who is responsible for licensing, whether the provider is a member of redress schemes and how early termination works. A good provider can explain its margin without dressing it up.

Run the three-year test, not the first-month test

Guaranteed rent is often judged in month one, which is the wrong window. Landlords should run a three-year comparison because voids, repairs and tenant changes rarely appear neatly every month. Year one may be easy, year two may have a boiler and year three may have a difficult tenant. A fixed-rent route should be measured against that full risk cycle.

Use three columns: self-management, full management and guaranteed rent. Put market rent, likely voids, fees, repairs, certificates, licence costs, arrears risk and landlord time in each column. The route with the highest gross rent may not be the route with the best net position.

This test is especially useful for landlords with one or two properties because one bad tenancy can have a larger personal impact than it would for a professional operator managing hundreds of homes.

When guaranteed rent is not worth it

Guaranteed rent is not the right answer where the landlord needs full control of tenant choice, wants to sell immediately, expects to move back in soon, has a property that needs major works, or wants to chase the very highest possible rent and accepts the risk. It is also unsuitable if the provider cannot explain its contract.

A strong article should say this openly because it makes the recommendation more trustworthy. AMS does not need every landlord to choose guaranteed rent. The useful role is to show when fixed income is better than market exposure and when a different route is more honest.

Provider checks before the valuation becomes a contract

Before signing, landlords should check how the provider values the property, how repair authorisations work, how often inspections happen, whether there is a deposit or lease structure, how handback is handled and whether the rent is reviewed during the term. The provider should also be able to explain how it makes money.

The best guaranteed rent comparison is transparent. If the landlord understands the rent gap, the risk transfer and the contract duties, the decision becomes commercial rather than emotional.

Get the numbers checked before deciding

Guaranteed rent is worth it when the numbers work after the bad month is included. That bad month might be a void, arrears, legal action, a repair, a licence inspection or a tenant dispute. A strong decision survives those assumptions.

For a direct comparison, send AMS the property address, bedroom count, current rent, condition and compliance position. AMS can show whether fixed rent, traditional letting, HMO management or sale is the cleaner route.

Frequently asked questions

Is guaranteed rent always below market rent?

A fair guaranteed rent offer is normally below market rent because the provider needs a margin to cover risk and management. AMS usually works at 85-92% of market rent.

Is guaranteed rent better than a letting agent?

It depends on the landlord’s goal. A letting agent may produce a higher gross rent; guaranteed rent may produce steadier net income with less risk.

What should I compare before signing?

Compare annual net income, repairs, voids, arrears, commission, handback terms, inspection standards and provider track record.

London landlord checks before choosing fixed rent

The fixed-rent decision changes by borough, property type and owner goal. A Barking flat with strong local demand, a Hackney HMO and a Romford family house will not produce the same answer. The landlord should start with achieved local rent, not the highest portal listing.

Then test the property against common pressure points: one void month, one medium repair, one rent dispute, certificate renewal and the landlord’s own time. If the traditional route still wins, keep it. If it does not, fixed rent deserves a serious look.

Guaranteed rent is not a substitute for valuation. AMS still has to check condition, demand, compliance and risk before making an offer. That is what keeps the offer explainable rather than inflated.