Key Takeaways:

- Guaranteed rent equals your property’s market rent minus a provider margin of 10-20%, meaning most London landlords receive 80-92% of market value.

- Seven factors determine your exact rate: location, property condition, EPC rating, bedrooms, local demand, lease length, and compliance status.

- Seasonal rental fluctuations, leasehold service charges, and proposed EPC minimum standards all feed into the calculation formula.

- The Renters’ Rights Act 2025 is increasing provider costs for non-compliant properties, widening margins for landlords who haven’t prepared.

- AMS Housing Group offers free property valuations with personalised guaranteed rent quotes — call 020 3793 2247 or request a valuation online.

A landlord in Redbridge recently told us he’d been quoted three different guaranteed rent figures by three different providers — and the gap between the highest and lowest offer was over £300 per month. Same property. Same postcode. Three very different numbers. His question was simple: how are these companies arriving at their figures?

It’s the question every landlord should ask. Guaranteed rent isn’t a number pulled from thin air. It’s the output of a structured calculation that weighs your property’s market value against the provider’s risk profile. Get those inputs right, and you can predict — and influence — where your offer lands.

This guide breaks down the exact methodology providers use, step by step. You’ll see the formula, the seven variables that shift your rate, seasonal factors most landlords overlook, and four worked examples using real London postcodes and current 2026 market figures. Whether you’re exploring how guaranteed rent works for the first time or comparing offers from multiple providers, this is the calculation deep-dive you need.

What Is Guaranteed Rent? A Quick Primer

Guaranteed rent is an arrangement where a property management company leases your property for an agreed term and pays you a fixed monthly rent — regardless of whether the property is occupied or the tenant has paid. The provider takes on the responsibilities of finding tenants, managing the property, handling maintenance, and absorbing void periods.

For landlords, it removes the two biggest financial risks in property: empty months and non-paying tenants. For a fuller explanation, read our guide on how guaranteed rent works in practice. This article focuses specifically on how that monthly figure is calculated.

Two common points of confusion worth clearing up. First, guaranteed rent is not the same as rent guarantee insurance. Insurance reimburses you after a tenant defaults. Guaranteed rent pays you whether a tenant is in place or not — fundamentally different products. Second, some landlords wonder whether guaranteed rent is just rent to rent by another name. There’s mechanical overlap — a company leases your property and sublets it — but guaranteed rent providers operate as regulated property managers with formal agreements, not informal middlemen.

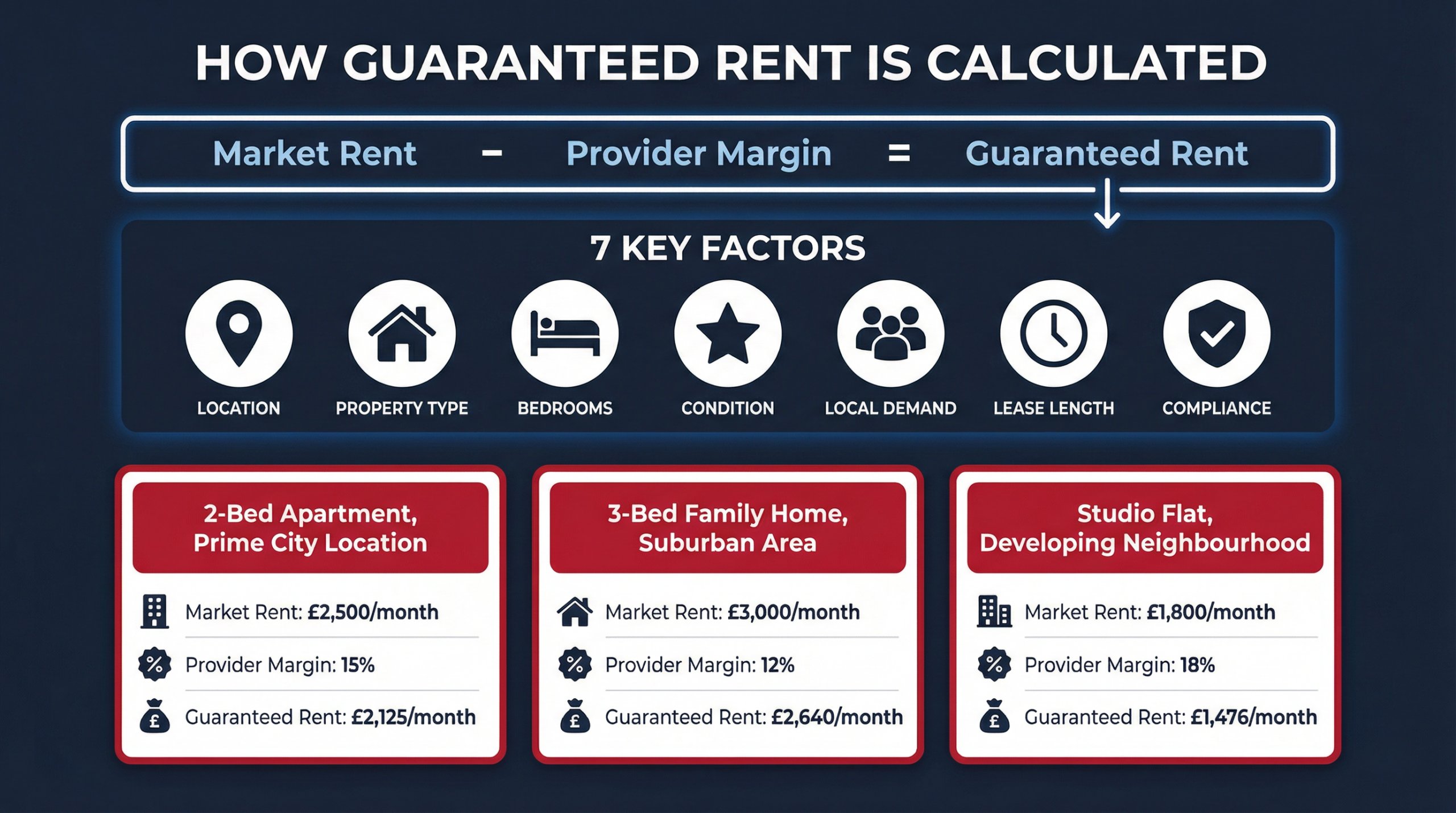

The Guaranteed Rent Formula

Every guaranteed rent calculation follows the same core logic:

Guaranteed Rent = Market Rent – Provider Margin

That margin typically falls between 10% and 20% of the market rent. It isn’t a fee you pay out of pocket — it’s built into the rate you’re quoted. The provider uses it to cover tenant sourcing, property management, repairs, void periods, compliance, and risk.

So if your property’s market rent is £1,800 per month and the provider applies a 12% margin, your guaranteed rent would be £1,584 per month. That £1,584 lands in your account on the same date every month for the duration of your agreement.

The real question is what determines where your margin sits within the 10-20% range. A low-risk property in a high-demand area with full compliance attracts a smaller margin and a better rate for you. A property that’s harder to let, needs investment, or carries regulatory gaps pushes the margin wider.

Once you understand how the amount is determined, our full guide on what guaranteed rent costs landlords breaks down the financial impact in detail — including five-year income projections and side-by-side comparisons with traditional letting.

Let’s walk through the five-step process providers use to arrive at your figure.

The 5-Step Guaranteed Rent Calculation Process

Step 1: Establishing Your Market Rent Baseline

Everything starts with what your property would realistically achieve on the open market right now. Not what you’d like it to fetch. Not what it earned two years ago. The current market rate, based on evidence.

Providers establish this through several channels:

- Comparable listings analysis — reviewing current asking rents and achieved rents for similar properties on Rightmove, Zoopla, and OpenRent in your postcode

- Recent lettings data — looking at properties that have actually let (not just been listed) in the past three to six months

- Local agent intelligence — cross-referencing with letting agents active in the area

- Portfolio experience — drawing on their own data from properties they already manage nearby

If you want to research your own baseline, our guide on how much you can rent your house for walks through how to run your own comparable analysis.

The market rent baseline is the single biggest input. Get this wrong and the entire calculation skews. That’s why reputable providers never rely on a single data source — they triangulate across multiple inputs to land on a defensible figure.

Step 2: Property Condition and EPC Assessment

A property in good condition is faster to let, attracts more reliable tenants, and costs less to maintain. All of that reduces provider risk — which translates directly into a better rate for you.

During the assessment, providers evaluate:

- General repair — walls, ceilings, windows, doors, roof condition

- Kitchen and bathroom — age, functionality, and overall standard

- Flooring and decoration — whether the property is tenant-ready or needs work before listing

- Fixtures and fittings — boiler age and service history, plumbing condition, electrics

- Outstanding maintenance — anything that would need fixing before a tenant moves in

The provider is calculating how much they’ll need to spend before the property generates income and how much ongoing maintenance will cost across the lease term. A property needing a £4,000 bathroom refit and a new boiler will see those costs reflected in a wider margin.

Understanding your full landlord responsibilities in the UK helps you see what providers are taking off your plate — and why the condition of what they’re inheriting matters so much to their pricing.

How Your EPC Rating Affects the Calculation

Your Energy Performance Certificate has become a genuine calculation factor in 2026, not just a compliance checkbox.

EPC C or above: This is the sweet spot. Properties rated A, B, or C face no regulatory risk under proposed Minimum Energy Efficiency Standards. Tenants prefer them because of lower energy bills. Providers price them favourably — expect the EPC factor to trim 1-2 percentage points off your margin.

EPC D: Acceptable for now, but providers know that regulatory pressure is building. If the government follows through on plans to require EPC C by 2030, a D-rated property represents a future compliance cost. That uncertainty gets priced in.

EPC E or below: Red flag territory. Properties rated E are at the current legal minimum for new tenancies, and anything below is unlettable. Providers either require an upgrade before agreeing terms or price the upgrade cost directly into a wider margin.

The maths is straightforward. Moving from D to C on a £1,800/month property could shift your margin from 16% to 14% — that’s an extra £432 per year in your pocket. Often the cost of improvement (loft insulation, LED lighting, draught-proofing, a smart thermostat) is under £1,000 and pays for itself within the first year.

Step 3: Location and Demand Analysis

London is not one rental market. Demand, void rates, tenant quality, and rental growth trajectories vary enormously by borough, and sometimes by individual postcode.

Providers assess:

- Transport connectivity — proximity to tube, Overground, Elizabeth line, and National Rail stations. Properties within a 10-minute walk of a station let faster.

- Employment centres — access to Canary Wharf, the City, Stratford, and other major employment hubs drives consistent tenant demand.

- Local amenities — schools, shops, green spaces, and healthcare facilities all factor in.

- Area trajectory — boroughs undergoing regeneration (think Barking Riverside, Beam Park, Thamesmead) attract tighter margins because rental growth is anticipated.

- Tenant demand patterns — some areas attract professional sharers, others attract families on housing benefit. The tenant profile affects void risk and management intensity.

- Competition density — how many comparable properties are available at any given time. A saturated market means longer void periods.

East London boroughs — Barking and Dagenham, Newham, Redbridge, Havering, Waltham Forest — have seen sustained demand partly driven by Elizabeth line connectivity, ongoing regeneration, and relative affordability compared to inner London. This consistent demand is one reason AMS Housing Group, which has operated across these boroughs since 2009, can often offer competitive margins.

Step 4: Risk and Cost Assessment

This is where the provider puts a price on uncertainty. They’re calculating the total cost of managing your property over the lease term and ensuring their margin covers it.

The risk assessment includes:

- Void period probability — based on local market data, how many weeks per year the property is likely to sit empty between tenancies. London averages around 3-4 weeks per void.

- Tenant turnover rate — how often tenants move on. Higher turnover means more void periods, more referencing costs, and more wear-and-tear.

- Maintenance budget — estimated annual spend on repairs, servicing, and eventual replacements. Older properties carry higher maintenance risk.

- Compliance costs — gas safety certificates, EICRs, fire risk assessments, landlord licensing fees, and any upcoming regulatory requirements.

- Insurance exposure — buildings and contents cover, public liability, and any specialist cover required for HMOs.

- Eviction risk — the cost and timeline of removing a problem tenant. With court possession averaging over 30 weeks in London, this is a material risk that providers price carefully. Our guide on how to evict a tenant in the UK covers the process and timeline in detail.

The provider is running a projected profit and loss for your property over the lease period. If the numbers work at a 12% margin, that’s what they’ll offer. If not, the margin widens until the risk is adequately covered.

Understanding all the costs landlords face helps you appreciate why providers need this margin — and why removing costs from the equation (through compliance, good condition, and long leases) directly benefits your rate.

Step 5: Contract Terms and Final Offer

The final step synthesises everything into a firm monthly figure. But the structure of the agreement itself also affects where the margin lands.

Lease length is the biggest lever here. A longer commitment gives the provider planning certainty — they can amortise upfront costs (decoration, marketing, compliance checks) over more months, reducing the per-month cost. Most providers offer agreements from one to five years.

- 12-month rolling — highest margins, because the provider faces re-negotiation risk annually

- 2-3 year fixed — moderate margins, a good balance for most landlords

- 5-year fixed — tightest margins, maximum certainty for both parties

Payment terms also matter. Some providers pay monthly in advance, others in arrears. Monthly in advance is standard and preferable — you know the money is coming before the month starts.

Renewal terms should be discussed upfront. Does the rate adjust at renewal? Is there an automatic renewal clause? What notice period applies? These details don’t change the initial calculation, but they affect the long-term value of the deal.

What Percentage of Market Rent Is Guaranteed Rent?

This is the question landlords search for most often, so let’s put clear numbers on it.

Private Company Rates

| Property Profile | Typical % of Market Rent | Margin |

|---|---|---|

| Excellent condition, high-demand area, EPC C+ | 88-92% | 8-12% |

| Good condition, strong area, EPC C-D | 85-90% | 10-15% |

| Fair condition, moderate demand, EPC D | 82-87% | 13-18% |

| Needs work, weaker area, EPC E | 78-85% | 15-22% |

| HMO, fully compliant, high demand | 88-92% | 8-12% |

The range is wide because no two properties are the same. A fully compliant, recently refurbished two-bed flat in a Zone 3 borough with Elizabeth line access sits at the top of the range. An older property with deferred maintenance in a slower market sits towards the bottom.

Council Guaranteed Rent Rates

Council-backed guaranteed rent schemes — sometimes called leasing schemes — work differently. Instead of market rent, they typically benchmark against Local Housing Allowance (LHA) rates.

LHA represents roughly the 30th percentile of local market rents. Council schemes may offer at or slightly above LHA, which can mean 70-90% of true market rent depending on your borough. The exact percentage varies by local authority, property size, and current demand for temporary accommodation.

If you’re considering this route, our guides on renting your property to the council and how much the council pays to rent your house break down the specifics.

Council schemes often include longer lease terms (3-5 years), guaranteed void-free occupancy, and full management. The trade-off is a lower headline rent compared to private providers.

How Contract Length Affects Your Percentage

Here’s how lease length typically shifts the margin, all else being equal:

| Lease Length | Typical Margin Adjustment |

|---|---|

| 12-month rolling | Baseline margin (no reduction) |

| 2-year fixed | 0.5-1% tighter than baseline |

| 3-year fixed | 1-2% tighter than baseline |

| 5-year fixed | 2-3% tighter than baseline |

On a property with a £2,000/month market rent, a 2% margin reduction from choosing a 5-year lease over a 12-month deal is worth £480 per year — or £2,400 over the full term. It’s a meaningful lever.

How Seasonal Market Rent Variations Affect Your Offer

Here’s something most guaranteed rent guides don’t mention: the time of year you request a valuation can influence your offer.

London’s rental market follows predictable seasonal patterns. Demand peaks between May and September, driven by graduate relocations, corporate moves, and family moves timed around the school year. Rents during peak season can run 5-8% higher than the winter trough (typically December to February).

How this affects your guaranteed rent calculation:

Providers don’t simply take a snapshot of rents on the day they value your property. They average across the seasonal cycle to arrive at a sustainable market rent figure. But there’s a subtlety here. If you request a valuation in July when comparable rents are at their peak, the evidence supports a higher baseline — even after seasonal smoothing.

Conversely, a January valuation captures the market at its weakest point. The provider may discount the baseline further to account for the fact that if they need to re-let the property in winter, they’ll face softer demand and potentially lower achievable rents.

Practical takeaway: if you can time your valuation for late spring or early summer, the market evidence will support a stronger baseline. It won’t transform a below-market offer into an above-market one, but it can edge your figure up by 2-3%.

Leasehold Properties: How Service Charges and Ground Rent Affect the Calculation

If your property is leasehold — and many London flats are — there’s an additional layer to the calculation that freehold landlords don’t face.

Service charges are a fixed annual cost that guaranteed rent providers must account for. They vary enormously: a small conversion flat might carry £1,200/year in service charges, while a purpose-built flat with a concierge, gym, and managed gardens could be £4,000/year or more.

Providers handle this in one of two ways:

- Gross approach — the guaranteed rent figure is quoted inclusive, and the provider pays the service charge out of their margin. This is simpler for the landlord but means the headline rent is lower.

- Net approach — the guaranteed rent is quoted exclusive of service charges, and the landlord pays them directly. This is more common and means a higher headline rent figure, but the landlord retains the service charge obligation.

Make sure you understand which approach your provider uses. A “higher” offer on a gross basis might actually be lower once you compare it net of service charges.

Ground rent is another consideration, though the Leasehold Reform (Ground Rent) Act 2022 capped ground rent at zero (a “peppercorn”) for new residential leases. If you hold a pre-2022 lease, you may still be paying ground rent of £200-£500/year. Providers factor this in as a cost of the arrangement.

Major works and sinking funds can also affect the calculation. If the provider knows that a major works programme is planned (roof replacement, cladding remediation, lift refurbishment), they’ll either widen the margin to absorb the risk or require the landlord to handle major works costs directly. This is always worth discussing upfront.

Worked Examples: Guaranteed Rent Calculations for Different London Properties

These examples use realistic 2026 London figures for properties across different boroughs. Your actual quote depends on a full property assessment.

Example 1: Two-Bed Flat in Walthamstow (E17)

| Element | Detail |

|---|---|

| Property | 2-bed purpose-built flat, E17 |

| Condition | Good — recently redecorated, modern fitted kitchen |

| EPC Rating | C |

| Compliance | All certificates current |

| Tenure | Leasehold (service charge £1,800/year paid by landlord) |

| Market Rent | £1,750/month |

| Provider Margin | 13% |

| Guaranteed Rent | £1,523/month (£18,276/year) |

Why 13%? Walthamstow has strong rental demand fuelled by Victoria line access and the growing appeal of “Awesomestow” as a lifestyle destination. The property is well-maintained with a good EPC, and all compliance documents are current. The leasehold structure means the landlord carries the service charge, but the net position is still strong. The single-occupancy structure (one tenancy rather than multiple rooms) keeps the margin slightly above the tightest range.

Example 2: Four-Bed Terraced House in Dagenham (RM10)

| Element | Detail |

|---|---|

| Property | 4-bed mid-terrace house, RM10 |

| Condition | Fair — functional but dated kitchen, original bathroom |

| EPC Rating | D |

| Compliance | Gas safety current, EICR expired |

| Tenure | Freehold |

| Market Rent | £2,200/month |

| Provider Margin | 17% |

| Guaranteed Rent | £1,826/month (£21,912/year) |

Why 17%? The property has several factors pushing the margin wider. The expired EICR is a compliance cost the provider absorbs immediately. The D-rated EPC creates future regulatory risk. The dated kitchen and bathroom mean higher maintenance costs and potentially slower letting. However, Dagenham benefits from Beam Park regeneration and improved transport links, which keeps the margin from pushing above 18%. A freehold property avoids the complications of service charges and leasehold restrictions.

Example 3: Six-Bed HMO in Ilford (IG1)

| Element | Detail |

|---|---|

| Property | 6-bed licensed HMO, IG1 |

| Condition | Very good — purpose-converted with en-suite rooms |

| EPC Rating | B |

| Compliance | Mandatory HMO licence, fire safety, gas, EICR — all current |

| Tenure | Freehold |

| Market Rent | £4,200/month (total across all rooms) |

| Provider Margin | 9% |

| Guaranteed Rent | £3,822/month (£45,864/year) |

Why 9%? This is about as tight as margins get. Six separate income streams spread void risk across multiple tenants — losing one occupant costs the provider one-sixth of income, not all of it. The property is purpose-converted with en-suites (the gold standard for HMO guaranteed rent), fully licensed, and carries a B-rated EPC. Ilford’s Elizabeth line access generates consistent demand for professional room lets. The result: minimal risk, minimal margin.

Example 4: Studio Flat in Stratford (E15)

| Element | Detail |

|---|---|

| Property | Studio flat (open-plan), E15 |

| Condition | Good — modern build, fitted kitchen, shower room |

| EPC Rating | B |

| Compliance | All certificates current |

| Tenure | Leasehold (service charge £2,400/year paid by landlord) |

| Market Rent | £1,350/month |

| Provider Margin | 15% |

| Guaranteed Rent | £1,148/month (£13,776/year) |

Why 15%? Stratford has excellent transport links and regeneration appeal, which supports demand. But studios carry inherent risk for providers: the tenant pool is narrower (singles and couples only), turnover tends to be higher as tenants outgrow the space, and each void period wipes out 100% of income. The modern condition and strong EPC offset these risks somewhat, but the structural limitations of a single-occupancy studio keep the margin in the mid-range.

The pattern across all four examples is consistent: the more risk you remove from the provider’s side — through compliance, good condition, strong demand, and diversified income — the less margin they need, and the more you keep.

How to Maximise Your Guaranteed Rent Offer

You can’t change your postcode, but there’s plenty you can do to push your rate towards the top of the range before requesting a valuation.

Get Compliance Sorted Before the Valuation Visit

If your gas safety certificate, EICR, EPC, and any required landlord licences are all current, the provider doesn’t need to price in the cost of sorting them out. Renew anything due within six months before you request a valuation. The cost of proactive renewal is almost always less than the margin increase you’d face. If you’re unsure what’s required, our guide on new landlord rules covers the latest regulatory requirements.

Improve Your EPC Rating

Moving from D to C can shift your margin by 1-2 percentage points. The improvements are often straightforward: loft insulation, LED lighting, a smart thermostat, draught-proofing, and cavity wall insulation. The cost is usually under £1,000 and pays for itself within the first year of a guaranteed rent agreement.

Present the Property at Its Best

A fresh coat of paint, clean carpets, and a tidy garden cost relatively little but signal to the provider that this is a well-maintained property with a landlord who takes care of things. First impressions during the assessment visit directly influence the condition score — and therefore the margin.

Offer a Longer Lease Term

If you’re comfortable committing to three or five years, say so upfront. As the contract length table above shows, a longer commitment can reduce your margin by 2-3 percentage points. AMS Housing Group offers flexible terms starting from twelve months, with the option to extend up to five years.

Time Your Valuation Strategically

As discussed in the seasonal section, requesting a valuation between April and August means the market evidence supports a higher baseline. It won’t change the fundamentals, but it can edge your offer up.

Provide Maintenance Records

A boiler service history, receipts for recent work, and evidence of regular upkeep give the provider confidence in lower future maintenance costs. It’s the kind of detail that nudges a margin from 16% down to 14%.

Consider HMO Conversion

If you own a larger property (four bedrooms or more) in a borough that supports HMO licensing, converting can substantially increase your guaranteed rent income. Per-room yield is higher, diversified tenants lower void risk, and margins tighten accordingly. Make sure you understand the licensing requirements before proceeding.

Use the AMS Guaranteed Rent Calculator

Want a quick estimate before committing to a full valuation? AMS Housing Group offers a free online guaranteed rent calculator on our service page. Enter your borough, property type, number of bedrooms, and general condition to get an indicative guaranteed rent range based on current market data.

The calculator gives you a ballpark figure in seconds. For a precise, bankable offer, you’ll want our property experts to visit in person. They assess condition and compliance, review local market data, and provide a firm offer — usually within 48 hours. No charge, no obligation.

Request a free valuation online or call us on 020 3793 2247.

How the Renters’ Rights Act Affects Guaranteed Rent Calculations

The Renters’ Rights Act 2025 — with key provisions taking effect from 2026 — is reshaping the risk landscape for landlords and providers alike. Here’s how it feeds into the calculation. For the full picture, read our dedicated guide on how the Renters’ Rights Act 2026 affects guaranteed rent.

Section 21 abolition removes the no-fault eviction route for traditional lettings. This makes self-managing riskier, because removing a problem tenant now requires proving specific grounds under Section 8 — a process that averages over 30 weeks through the courts. For a full breakdown of the current eviction process and timeline, see our guide on how to evict a tenant in the UK. Guaranteed rent agreements typically operate as company lets rather than ASTs, so Section 21 changes don’t directly apply to the landlord-provider relationship. But providers face increased difficulty and cost when removing sub-tenants, and that risk filters into margins.

Mandatory PRS Ombudsman membership adds a new compliance cost. Landlords who fail to register face penalties of up to £7,000. Providers factor this into their cost base, alongside existing gas safety, EICR, fire safety, and licensing requirements.

Periodic tenancies as default means providers can no longer lock sub-tenants into long fixed terms. Higher potential tenant turnover increases void risk and management costs, which feeds into the margin calculation.

The Decent Homes Standard is another incoming requirement. Rental properties will need to meet a defined standard covering structural integrity, damp, heating, and kitchen/bathroom facilities. Properties that already meet this standard face no extra cost. Those that don’t will see providers pricing remediation into wider margins.

The practical impact on your guaranteed rent:

Properties that are already fully compliant see minimal impact — the regulatory changes don’t create new costs for them. Properties with compliance gaps face wider margins as providers price in the cost of bringing them up to standard and managing them under the new landlord rules.

The landlords getting the best guaranteed rent rates in 2026 are those with compliant, well-maintained properties in high-demand areas on longer lease terms. The Act widens the gap between well-prepared landlords and those who haven’t kept pace.

How AMS Housing Group Calculates Your Guaranteed Rent

AMS Housing Group has been providing guaranteed rent across London since 2009, currently managing over 500 properties. Here’s how our calculation process works.

Step 1: Initial enquiry. You contact us by phone (020 3793 2247), through our online valuation form, or via our guaranteed rent calculator. We gather basic details: address, property type, bedrooms, and your current situation.

Step 2: Market analysis. Before visiting, our team runs a full market rent assessment using portal data, recent lettings in your postcode, and our own portfolio intelligence. We arrive at your property with a clear picture of the local market.

Step 3: Property inspection. One of our property experts visits to assess condition, compliance status, EPC rating, and any factors that would affect lettability. This is thorough but not intrusive — typically 30-45 minutes.

Step 4: Calculation and offer. We synthesise market data, property factors, and our operational cost model to calculate a sustainable guaranteed rent figure. You receive a firm, written offer — usually within 48 hours of the inspection.

Step 5: Agreement. If the offer works for you, we agree terms (lease length, payment dates, responsibilities) and move to contract. If it doesn’t, there’s no charge and no pressure.

What’s included in the AMS guaranteed rent margin:

- Full property management at 0% commission

- Inspections every four to six weeks

- Free inventory and check-in/check-out

- Minor repairs and maintenance at no extra cost

- Tenant sourcing, referencing, and management

- Compliance management (gas safety, EICRs)

This means the headline guaranteed rent figure is genuinely what you receive — there are no additional management fees eating into your income.

Common Mistakes When Evaluating Guaranteed Rent Offers

Comparing Headline Figures Without Accounting for What’s Included

Provider A offers £1,600/month but charges 12% management fees on top. Provider B offers £1,450/month with full management included. Provider B’s net figure (£1,450) beats Provider A’s (£1,408) — but most landlords choose A because the headline looks better. Always compare net of all fees. Don’t fall for the common myths about rent guarantees that circulate online — headline comparisons without context are one of the biggest.

Overestimating Your Market Rent Baseline

Setting your expectations based on the highest asking rent in your postcode rather than achieved rents leads to disappointment. Providers base their calculations on what properties actually let for, not aspirational listing prices that sit on Rightmove for weeks.

Ignoring the Value of Guaranteed Income

A guaranteed £1,500/month for 12 months is £18,000. A market rent of £1,700/month with a four-week void and one month of arrears is £15,300. The “lower” guaranteed figure often delivers more actual income over a year. For a deeper look at this comparison, see our guide on whether guaranteed rent is worth it.

Not Getting Multiple Quotes

The landlord in Redbridge I mentioned at the start received offers ranging from £1,400 to £1,720 for the same property. Different providers have different cost bases, risk appetites, and business models. Getting three quotes takes minimal effort and can be worth thousands over a lease term. Our guide on choosing the right guaranteed rent provider walks through what to look for beyond the headline number.

Neglecting to Read the Exit Terms

A strong monthly rate means nothing if you’re locked into unfavourable exit terms. Check the notice period, break clauses, and what happens if the provider defaults. Three months’ notice on either side is standard. Anything longer should raise questions.

Frequently Asked Questions

What percentage of market rent do guaranteed rent schemes pay?

Most private guaranteed rent companies pay 80-92% of market rental value. The exact percentage depends on property condition, location, EPC rating, and lease length. Well-maintained properties in high-demand London boroughs with strong compliance can achieve 88-92%. Properties needing work or in slower markets may receive 78-85%.

How is guaranteed rent different from rent guarantee insurance?

Guaranteed rent is a lease arrangement where a company pays you fixed rent whether the property is occupied or not. Rent guarantee insurance is a policy that reimburses lost rent after a tenant defaults — you still self-manage, still face voids, and must claim after the event. They solve different problems. Learn more about how rent guarantee insurance works.

Can you negotiate a guaranteed rent offer?

Yes. If you can demonstrate strong compliance, offer a longer lease term, provide evidence of recent improvements, or show the property is in better condition than initially assessed, you have grounds to negotiate a tighter margin. Providers want your property — a conversation about the rate is expected and normal.

Does property condition affect guaranteed rent?

Significantly. A well-maintained property with a modern kitchen, good bathroom, and no deferred maintenance can receive 3-5 percentage points more than a comparable property in poor condition. The provider’s maintenance budget is one of the largest components of their margin — reduce it and your rate improves.

Is guaranteed rent taxable in the UK?

Yes. Guaranteed rent is treated as rental income by HMRC and must be declared on your Self Assessment tax return. You can still claim allowable expenses (mortgage interest relief at the basic rate, insurance, property management costs). The tax treatment is the same as traditional rental income.

How long are guaranteed rent contracts?

Most providers offer agreements from 12 months to 5 years. Shorter contracts give flexibility but attract wider margins. Longer contracts (3-5 years) typically secure better rates because they give the provider operational certainty. AMS Housing Group offers flexible terms from 12 months, with options to extend.

Does the council offer guaranteed rent?

Yes. Many London boroughs operate guaranteed rent or leasing schemes, often managed through housing associations or directly by the council. These schemes typically pay at or near LHA rates (the 30th percentile of local market rents), which can be 10-30% below private provider rates. The trade-off is longer leases, guaranteed occupancy, and full management. See our guide on renting your property to the council for borough-specific details.

What happens at the end of a guaranteed rent contract?

At contract end, you have three options: renew with the same provider (often at a renegotiated rate reflecting current market conditions), switch to a different provider, or return to self-managing or traditional letting through an agent. AMS Housing Group provides notice well before contract expiry so you have time to evaluate your options. There’s no penalty for choosing not to renew.

Get Your Personalised Guaranteed Rent Valuation

The only way to know exactly what your property could earn under guaranteed rent is a proper assessment. AMS Housing Group has been providing guaranteed rent across London since 2009, managing over 500 properties for landlords who want reliable income without the management burden.

- Free property assessment — our experts visit your property and review condition, compliance, and local market data

- Personalised quote — you receive a firm guaranteed rent offer, typically within 48 hours

- No obligation — if the rate works for you, we move forward. If not, no pressure and no charge

Don’t leave money on the table by guessing what your property is worth. Many of the landlords we work with discover their guaranteed rent figure is higher than they expected — especially after we factor in the void periods, maintenance costs, and management fees they’d face without it.

Try our free guaranteed rent calculator for an instant estimate.

Request a free valuation or call us on 020 3793 2247 to speak with a property expert today.